AI in Insurance Industry: What’s Driving Change in 2026

Date

May 25, 26

Reading Time

9 Minutes

Category

AI in Insurance

Share

The AI in insurance market sits at $718.9 million in 2026. By 2035, it hits $2.28 billion a 15.3% CAGR. And here's the thing: that's not a forecast built on optimism. That's capital already moving, deals already signed, infrastructure already being built.

So why are fewer than 22% of insurers actually running AI at scale?

Most are stuck in pilot purgatory. Some have been running the same pilot for two years straight. With the same dataset, the same small team, the same weekly status call where nobody pulls the trigger. Meanwhile, the insurers who did make the jump?

They've delivered 6.1x the total shareholder return of laggards over five years. Not a slight edge. Not a better quarter. A completely different business category.

The role of AI in insurance has quietly crossed a line - from "let's explore this" to "this is how we operate now." The real question isn't whether to use AI. It's why so many companies are still asking that question.

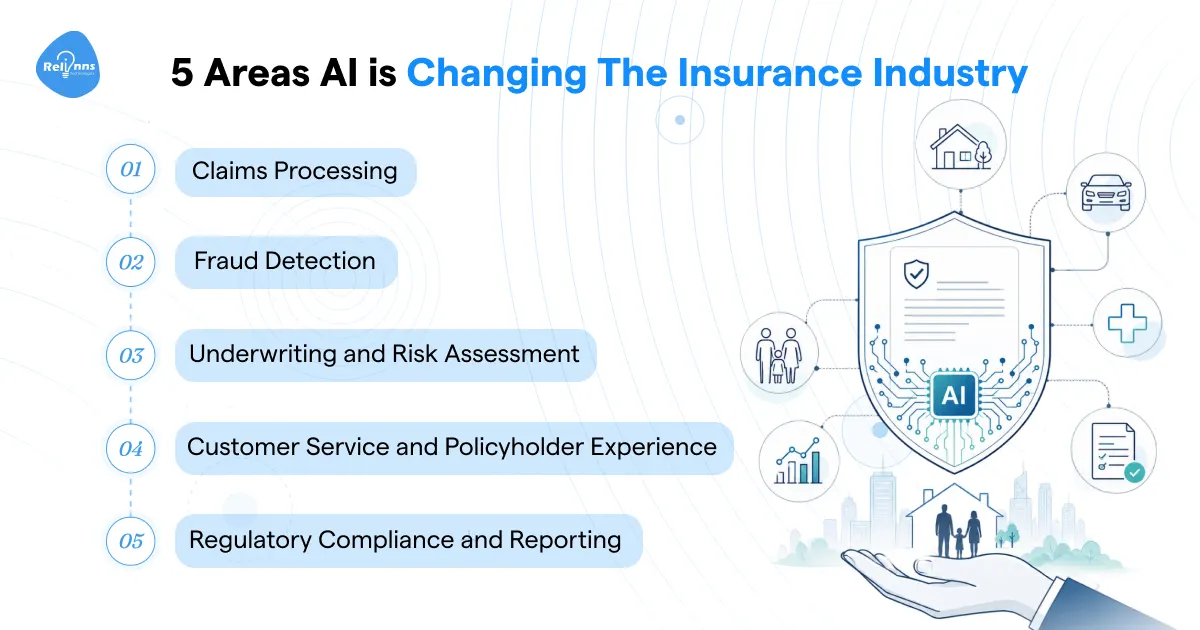

The Five Areas Where AI Is Moving the Numbers

There are five areas where AI stops being a slide deck and starts showing up in the P&L:

Claims, Fraud, Underwriting, Customer Service, and Compliance.

These aren't the flashiest use cases. They're chosen for a much simpler reason: they're where insurers bleed money every single day, quietly and consistently.

Here's what makes most pilots fail: companies either pick the wrong area to start, or they try to tackle all five at once and end up with five half-finished experiments and zero results. The insurers in that top 22%? They pick one area, rebuild it properly from the ground up, prove the return, then move to the next.

Let's walk through what AI leaders are actually doing inside each of these five areas not what they're testing, but what's working.

1. Claims Processing

Claims is where most insurers feel the pain first. Hundreds of documents come in every day. Adjuster notes, medical records, police reports. Someone reads all of it, pulls out what matters, routes the file, then writes a customer communication. Multiply that by your daily volume and you start to see why claims ops is where headcount quietly balloons.

LLMs changed this. An AI system now reads a full claim file and surfaces a synthesized summary in seconds. Computer vision assesses damage from photos without a physical inspection. Complexity scoring routes the file to the right adjuster before a human even opens it. Standard claims go through Straight-Through Processing with zero human touch.

The numbers back this up:

- Aviva deployed 80+ AI models across claims, cut liability assessment time for complex cases by 23 days, improved routing accuracy by 30%, dropped customer complaints by 65%, and saved over £60 million in 2024 alone

- Lemonade handles 55%+ of all claims with no human intervention and runs a Loss Adjustment Expense ratio of ~7% , roughly half the industry average

- AI-driven STP now accounts for 38% of all motor insurance claims globally

The role of AI in insurance claims isn't to replace adjusters. It's to stop them from spending their day reading PDFs.

Relinns builds AI Voice Agents for FNOL intake over phone, AI Chatbots for claim status queries, RAG systems for adjuster copilots, and custom AI for complexity scoring and routing.

2. Fraud Detection

Insurance fraud costs the industry at least $40 billion a year. And the problem is getting worse, not better. Fraudsters now use GenAI to produce synthetic documents, deepfake photos, and AI-written claim narratives that look completely legitimate to a human reviewer. The pattern-matching tools most carriers built three or four years ago weren't designed for this. They're not catching it.

The shift happening in AI for insurance industry fraud teams is from pattern-matching to semantic understanding. Modern systems read the full context of a claim narrative to catch subtle inconsistencies in causality and language that no keyword rule would flag. They run multimodal analysis, cross-referencing what a photo shows against what the written claim says. And they map hidden relationships across thousands of claims simultaneously to surface fraud rings that would take a human investigator months to find manually.

The results are real:

- Allianz deployed an AI fraud platform and saw a 29% increase in fraud detection

- Liberty Mutual hit a 4x increase in annual recoveries and a 20x improvement in fraud detection accuracy

- Across the industry, leading deployments have cut overpayment rates from ~10% down to low single digits and pushed detection accuracy up by more than 40%

One honest caveat here: These systems still need good historical claims data to train on. If your data is siloed or inconsistent, the model's output will reflect that. Clean data first. Then the model.

Relinns builds custom AI fraud scoring models, AI Agents for anomaly flagging inside claims workflows, and RAG layers over historical claims data for adjuster reference.

3. Underwriting and Risk Assessment

Traditional underwriting has a fundamental problem. It prices risk based on who you were, not who you are. The data is historical. The risk profile it produces is static. And by the time a customer's actual behavior could change their premium, it's already renewal season.

Real-time data broke that model open. Telematics in vehicles, IoT sensors in buildings, wearables tracking health data. The insurers taking AI in insurance seriously are using this data to price risk dynamically, not annually.

Usage-Based Insurance is the clearest example. Telematics tracks actual driving behavior, speed, braking, time of day, and AI prices the policy around it. Safer drivers pay less. Riskier ones pay more. The insurer stops cross-subsidizing bad behavior through pooled pricing. Beyond UBI, AI for insurance industry underwriting teams now use AI copilots that query policy rules, precedent cases, and underwriting guidelines in real time, cutting the time a complex application sits in a queue.

There's a subtler shift too. One North American insurer used AI to surface the implicit judgment calls their senior underwriters had been making for years, codified them into rules, and applied them consistently across the entire team. That's the kind of institutional knowledge that normally walks out the door when someone retires.

The numbers:

- CNP Assurances automated health questionnaire analysis, increased automatic acceptance rate by 5%, and cut onboarding time significantly

- Predictive analytics now influences 74% of underwriting decisions in life and health

- Risk assessment accuracy has improved 35% over traditional actuarial methods

Relinns builds custom AI for underwriting assistance, RAG systems over underwriting guidelines and policy documents, and AI Agents for multi-step application processing.

4. Customer Service and Policyholder Experience

Your contact centre volume isn't random. It spikes after every major weather event, every hospital admission, every accident. And the calls coming in? Mostly the same four or five questions, asked by different people, handled by agents who could be doing something harder.

The cost of staffing for peak volume is one of the most quietly expensive problems in insurance ops. And it's almost entirely solvable.

AI Voice Agents now handle inbound calls for renewal reminders, FNOL intake, claim status, and policy FAQ without a human in the loop. AI Chatbots cover the same ground on web and WhatsApp, around the clock. Here is how it looks like in practice:

- One carrier deployed a 24/7 AI chatbot for after-hours service and saw an 11% increase in policy purchases from prospective customers.

- Another used AI to generate 50,000 daily claims communications and found them clearer and more empathetic than what their human agents were writing.

- A third moved 80% of sales transactions online after implementing intelligent automation, and NPS scores rose 36 points.

For teams deploying AI in insurance customer ops, the chatbot layer is where most start. Relinns builds these on BotPenguin, a platform that deploys across 10+ channels including WhatsApp, Instagram, and web from a single dashboard, currently serving 50,000+ customers across 193 countries. For policy FAQ, claim status queries, and renewal workflows, it's a practical, fast-to-deploy starting point.

In UAE, Saudi Arabia, and Qatar, this matters even more. WhatsApp is where your customers already are. Renewal reminders, document collection, claim status updates over WhatsApp don't just reduce call centre volume. They get responded to. Relinns' WhatsApp AI Solutions are built specifically for this context, where an app download creates friction and a WhatsApp message doesn't.

58% of U.S. insurers have already deployed AI-driven chatbots handling 45% of initial inquiries without human involvement. The AI for insurance industry customer ops playbook is written. Most teams just haven't run it yet.

5. Regulatory Compliance and Reporting

Compliance used to be a documentation problem. Keep records, file reports, audit annually. Manageable with the right team.

It's not that anymore. The NAIC Model Bulletin and the EU AI Act now require insurers to document and justify their AI model outputs, not just their underwriting decisions. Every automated claim rejection needs a paper trail. Every AI-assisted pricing decision needs to be explainable to a regulator. Most compliance teams aren't built for this, and bolting it on manually after the fact is expensive and unreliable.

AI handles this at the layer where it matters. NLP reviews policy documents against current regulatory standards. Explainable AI frameworks produce justifiable, auditable outputs for every automated decision. Audit trails log every agent action automatically. When regulations change, AI monitors the update and drafts the internal communications needed to respond.

The numbers show where AI in insurance compliance is heading:

- 61% of global insurers are focused on Explainable AI specifically to justify automated claims rejections to regulators.

- 54% are investing in XAI frameworks to make their automated decisions fully auditable. And compliance costs have risen 24% for firms trying to implement AI/ML in insurance without proper governance infrastructure in place. That last one matters: the cost of not building compliance in from the start is higher than building it right.

Relinns builds custom AI for compliance documentation and audit trail layers, RAG systems over regulatory documents and internal policy libraries, and its Insurance Platform includes compliance-aware architecture from the ground up.

What Separates Insurers Who Get ROI From Those Who Don't

Most AI pilots in insurance don't fail because the technology doesn't work. They fail because the project was scoped wrong from the start.

The pattern looks like this: a team picks a low-stakes use case, builds a chatbot that answers basic policy questions, declares it a success, and then wonders six months later why nothing has changed in the P&L.

Layering AI on top of a broken workflow doesn't fix the workflow. It just makes the broken parts move faster.

McKinsey's research on this is direct. Transforming an entire domain, say all of claims end-to-end, produces double-digit P&L improvements. Isolated use cases don't move the needle.

The insurers seeing 10 to 20% improvement in new-agent success rates, 10 to 15% premium growth, and 20 to 40% reductions in onboarding costs aren't running one-off pilots. They've rebuilt how a full function operates.

Three specific failure modes show up repeatedly:

Data isn't AI-ready.

49% of insurance organizations are running on legacy systems over 12-15 years old. An AI model trained on fragmented, siloed, or inconsistent claims data will produce fragmented, inconsistent outputs. The model isn't the problem. The data is.

Off-the-shelf models don't know your business.

A generic LLM doesn't understand your underwriting philosophy, your claims adjudication rules, or your specific risk appetite. It needs to be trained on your data, your guidelines, your edge cases. That's not a vendor pitch. That's just how AI/ML in insurance models actually work.

No one planned for adoption.

McKinsey puts it plainly: change management represents half the effort required to secure AI ROI. You can build the best claims intelligence tool in the market and watch it sit unused because adjusters weren't brought into the process and don't trust the output.

The insurers getting real returns from AI in insurance didn't stumble into it. They picked one domain, rebuilt it properly, measured it, and then moved.

The AI Stack an Insurer Actually Needs

Forget the vendor catalogues. There are really three layers of AI in insurance technology, and each one does a different job.

- The conversational layer is customer-facing. Voice agents, chatbots, WhatsApp flows. This is what your policyholders interact with when they call about a claim, ask about their coverage, or need a renewal reminder. It reduces contact centre volume and improves response times. It's the fastest layer to deploy and the easiest to measure.

- The decision layer is adjuster-facing and underwriter-facing. RAG systems that make your policy documents and claims SOPs instantly queryable. Custom AI models that score claim complexity or flag fraud. Fine-tuned LLMs that understand your specific underwriting guidelines, not just the general concept of insurance. This layer is where AI for insurance industry operations actually changes how work gets done, not just how customers get answered.

- The workflow layer is operations-facing. AI agents that run multi-step processes end-to-end without a human hand-off between each step. Think FNOL intake to routing to communication drafting, all connected. Or application processing from submission to underwriting decision. This is where AI/ML in insurance goes from tool to infrastructure.

Most insurers start at the conversational layer. That's fine. But stopping there is why so many pilots produce activity metrics with no P&L impact. The decision and workflow layers are where the numbers change.

Each layer builds on the one below it. Conversational AI that can't hand off to a decision layer just creates a better FAQ page.

Relinns builds across all three layers for insurance operators.

AI in Insurance by Sub-Sector: Where It Applies Most

Not every insurer has the same starting point. Here's where AI in insurance maps most directly to each sub-sector.

Life Insurance

Life insurers spend a disproportionate amount of time on health questionnaire processing and manual underwriting reviews. AI automates both. CNP Assurances is a real example: automated questionnaire analysis increased their automatic acceptance rate by 5% and cut onboarding time significantly.

AI now accounts for 28% of total insurance AI application usage in the life segment, with projected growth of 29.5%. The bigger opportunity is policy personalization, using wearable and health data to offer coverage that actually reflects an individual's current risk, not their demographic profile.

Health Insurance

Pre-authorization is one of the most operationally painful processes in health insurance. It requires back-and-forth between the hospital, the insurer, and the patient, and it's almost entirely manual. AI handles document intake, cross-references policy coverage rules, and flags exceptions for human review.

What's more, AI for insurance industry health teams are using population health models to identify high-risk members before a major claim event, which changes the economics of the whole book.

General Insurance (Motor, Home, Travel)

Car insurance is the largest AI application segment at 38% of the market, growing at 33.1%. Telematics-based pricing is the main driver. For property, 59% of firms now use drone imagery and AI for post-disaster damage assessment, cutting physical inspection requirements and accelerating settlements.

Property insurance AI sits at 22% market share with 27.8% growth. Travel and marine are smaller but catching up as AI/ML in insurance models get better at pricing short-duration, high-variability risk.

InsurTech and Neo-Insurance

This is where the framing flips. For InsurTechs, AI in insurance industry operations isn't a layer on top of existing processes. It's the core architecture.

Lemonade is the clearest example: AI handles 55%+ of claims with zero human intervention, and their cost structure reflects it. If you're building a new insurance product or distribution model, starting without AI embedded at the foundation means you're already behind on unit economics.

Where This Leaves You

The insurers pulling ahead aren't the ones with the most AI tools. They picked one or two operations that were bleeding cost or losing customers, rebuilt those workflows around AI, and measured what changed.

Claims processing that took weeks now takes hours. Fraud that slipped through pattern-matching tools gets caught at FNOL. Underwriters spend time on complex cases instead of reading PDFs. Contact centres stop staffing for peak volume because AI handles it.

The Technology isn't the bottleneck. Picking the right starting point is.

Relinns builds AI systems for insurance operators, from AI Voice Agents for FNOL intake to custom claims intelligence platforms, RAG systems over policy libraries, and WhatsApp AI Agents for GCC markets where that's where your customers already are. If you want to see what this looks like for your specific operation, book a 30-minute insurance-specific demo with the Relinns team.

Sources: