AI in Life Insurance: Everything You Need To Know in 2026

Date

May 26, 26

Reading Time

14 Minutes

Category

AI in Insurance

Share

Renewal calls stack up. Claim queues overflow after every major hospital event. Pre-auth bounces between three parties with no clear owner, and agents spend hours on work that doesn't need a human.

That's the real cost of running on manual workflows.

AI in life insurance is closing that gap. And carriers using AI in life insurance are showing it in revenue, retention, and speed. This blog covers where artificial intelligence in life insurance moves the needle, from underwriting to claims to ops.

What Is AI and Its Core Technologies

At its simplest, AI is software that learns from data, spots patterns, and makes decisions without needing a human to spell out every rule. That's it. No magic.

The technologies doing the heavy lifting are machine learning (finds patterns in historical data), natural language processing (reads and understands text and speech), predictive analytics (forecasts what's likely to happen next), and generative AI (creates content, summaries, and responses on demand).

Now, why does artificial intelligence in life insurance fit so well? Because the industry runs on exactly the kind of data these tools are built for. Policy documents, claim histories, medical records, customer calls. It's all structured, repeatable, and high-volume.

AI in life insurance doesn't replace judgment. But it does read 10,000 applications faster than any team can, flag the ones that need attention, and handle the rest. Insurance AI agents are already doing this at scale. That's the baseline we're working from.

The Growing Role of AI in Transforming Life Insurance

A few years ago, most carriers were running AI in controlled pilots, carefully watching one use case while the rest of the business ran the same way it always had. That phase is over.

AI in life insurance has moved into production. John Hancock and Haven Life have shifted to real-time underwriting models that assess risk dynamically, not through a weeks-long manual review. Insurance AI agents now handle thousands of service requests daily without adding a single headcount.

The three areas feeling it most: underwriting speed, customer personalization, and operational efficiency. These aren't adjacent improvements. They compound. Faster underwriting means faster revenue. Better personalization means lower churn. Leaner ops means you can scale without the cost base growing at the same rate.

But faster approvals and lower overhead are just the surface. The bigger shift is what artificial intelligence in life insurance does to sales, and where it actually stops them from happening.

Key Statistics and Trends in AI Adoption in Life Insurance

The numbers tell a clear story.

- AI implementation in life insurance hit 48% in 2025, up from 29% the year before.

- Over 50% of carriers are now piloting or deploying generative AI for agent workflows.

- McKinsey puts the return gap at 6.1x higher for top AI adopters, with 10 to 15% premium growth and onboarding costs down by 40%.

- BCG projects a 15 to 22% profit increase for AI-first insurers by 2028.

The share of insurers still just "considering" AI dropped from 51% in 2021 to 42% in 2025. The window for watching from the sidelines is closing.

Where Most Life Insurance Sales Are Actually Lost

Most carriers pour budget into lead generation. Ads, broker networks, referral programs. And then lose the sale somewhere much less visible.

1. Speed to First Contact

A prospect who gets a response within 5 minutes is 100 times more likely to convert than one contacted 30 minutes later. That's not a small edge. That's a different game entirely.

Most agents are still manually dialing through a list while a competitor's AI for life insurance agents has already sent a personalized response, booked a call, and pre-qualified the lead. By the time your agent picks up the phone, the conversation has already started somewhere else.

2. Follow-Up Drop-Off

The average agent stops following up after 2 or 3 touches. Sales in life insurance regularly close between touch 5 and touch 8.

That gap is where deals die quietly. Manual follow-up gets deprioritized the moment the pipeline gets busy, which means the leads you paid to acquire just go cold. Automated multi-touch sequences don't forget. They don't get distracted. They keep the cadence going until the prospect responds or opts out.

3. Post-Meeting Execution

Discovery calls are where the sale is decided. They're also where the most information gets lost.

Agents leave with scattered notes, half-remembered details, and a vague plan to "write it up later." What follows is either a generic proposal that misses what the client actually said, or a NIGO submission that stalls underwriting and frustrates everyone involved.

NIGO (Not In Good Order) submissions are one of the most expensive and avoidable delays in the policy issuance process. AI in life insurance fixes this by capturing what was said in the meeting, structuring it into a formatted summary, and pushing the relevant data directly into the CRM. The proposal reflects the actual conversation. The submission goes in clean the first time.

That's not a marginal improvement. That's the difference between a policy placed and a prospect who moves on.

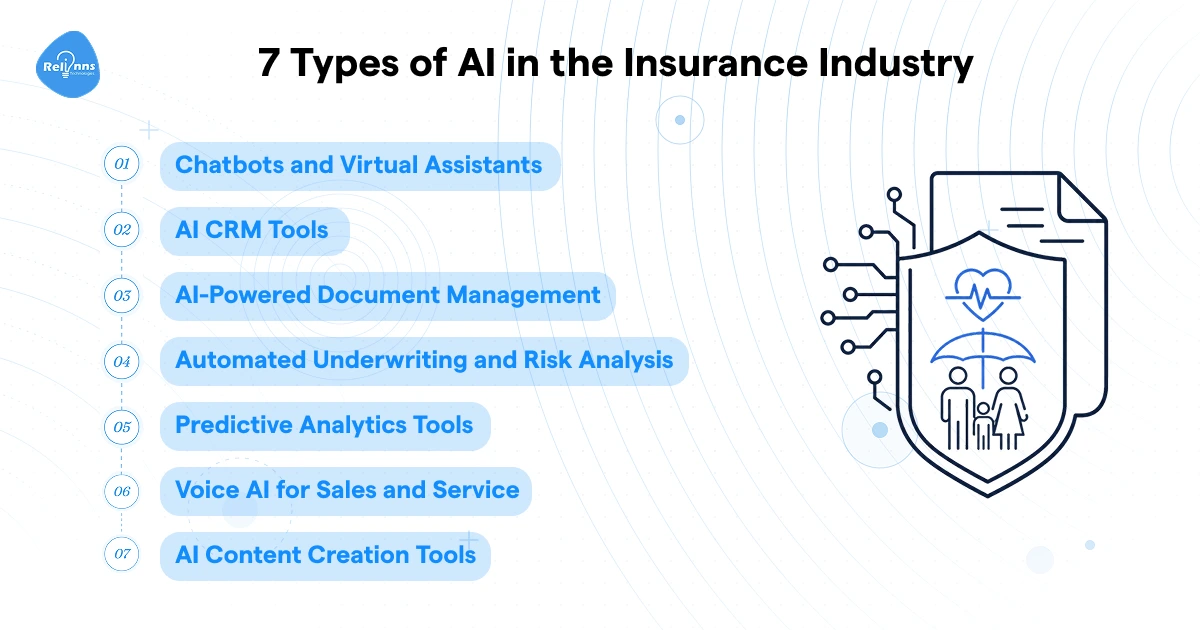

Types of AI in the Insurance Industry

AI in life insurance isn't one thing. It's a stack of different tools, each solving a different problem. Here's what's actually out there.

1. Chatbots and Virtual Assistants

These handle the repetitive front-line work: routine queries, instant quotes, appointment scheduling, all outside business hours. Insurance AI agents running on your website or CRM keep leads engaged while your team focuses on complex cases that actually need a human.

2. AI CRM Tools

CRM platforms with built-in AI analyze client behavior, flag churn risk, and surface the right moment to reach out. For an AI for life insurance agent managing a large book of business, this is the difference between reactive and proactive account management.

3. AI-Powered Document Management

Forms, applications, ID verification, claims documents. AI reads them, extracts the data, validates it, and flags inconsistencies in real time. What used to take hours of back-and-forth now clears in minutes.

4. Automated Underwriting and Risk Analysis

This is where artificial intelligence in life insurance has the clearest operational impact. Models pull in health data, credit scores, and behavioral signals and return a risk assessment in seconds. Pricing gets sharper. Policy issuance speeds up. And the model keeps improving as more data flows through it.

5. Predictive Analytics Tools

These tools spot patterns your team would miss. Which customers are about to lapse. Which leads are most likely to convert. Which renewal conversations to prioritize this week. Churn that felt unpredictable becomes something you can get ahead of.

6. Voice AI for Sales and Service

Voice AI sits on top of calls and works in real time. It picks up sentiment shifts, surfaces relevant talking points, flags upsell signals, and gives agents coaching cues mid-conversation. High-volume phone teams see the biggest lift here.

7. AI Content Creation Tools

Proposal drafts, follow-up emails, policy summaries. AI generates the first version fast and keeps the tone consistent across every touchpoint. It's not replacing good writing. It's removing the blank-page problem so agents spend time refining, not starting from scratch.

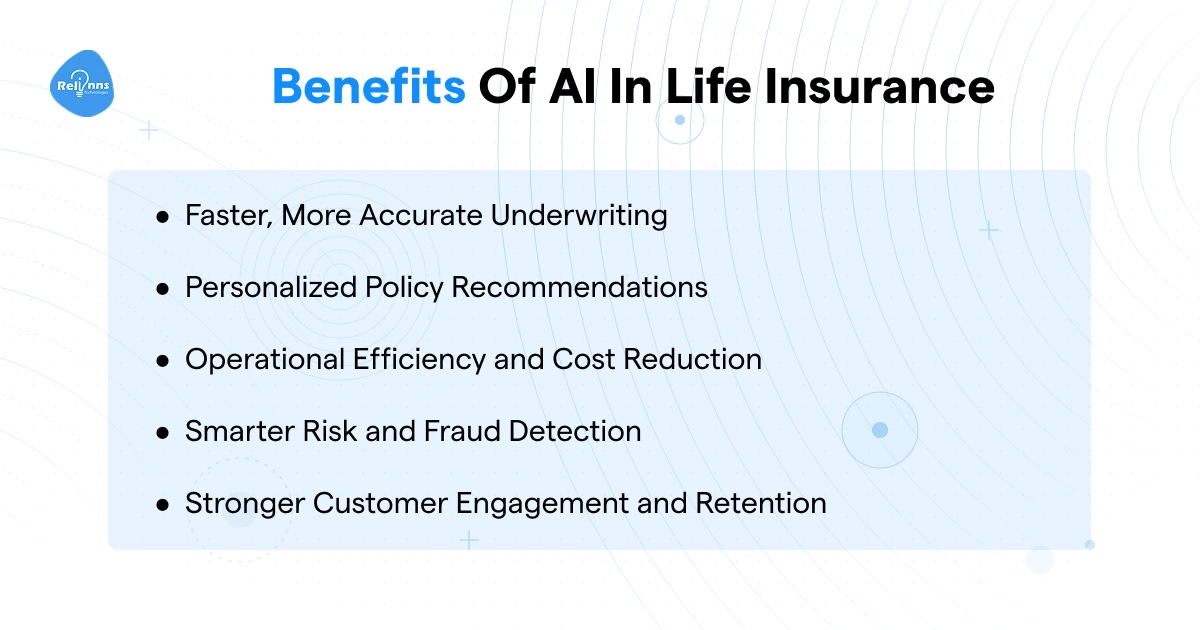

Benefits of AI in Life Insurance

Faster processes and lower costs sound good on paper. But the real question is what they actually change inside the business. Here's where artificial intelligence in life insurance pays off in ways you can measure.

1. Faster, More Accurate Underwriting

Decisions that used to take two to three weeks now take minutes. The models don't just run faster, they get more accurate over time as more data flows through them. And because rules apply consistently across every application, you remove the variability that comes from different underwriters reading the same case differently.

2. Personalized Policy Recommendations

AI in life insurance analyzes demographics, financial behavior, and life stage in real time and matches products accordingly. That match improves as the customer's profile changes. Which means you're not just converting better at the start, you're cross-selling more effectively over the full relationship.

3. Operational Efficiency and Cost Reduction

Data entry, claims triage, renewal reminders. These are high-volume, low-judgment tasks that eat team capacity. Automating them doesn't just cut costs, it frees your people for work that actually needs human judgment. You handle more volume without adding headcount.

4. Smarter Risk and Fraud Detection

Insurance AI agents running anomaly detection across applications and claims catch inconsistencies that manual review misses. Early flags mean you intervene before a payout, not after. Compliance and governance get tighter as a side effect.

5. Stronger Customer Engagement and Retention

Policyholders who get timely, relevant communication stay longer and buy more. AI tracks behavior across the lifecycle and triggers the right message at the right moment. Renewal rates go up. Churn goes down. And it happens without your team manually managing every touchpoint.

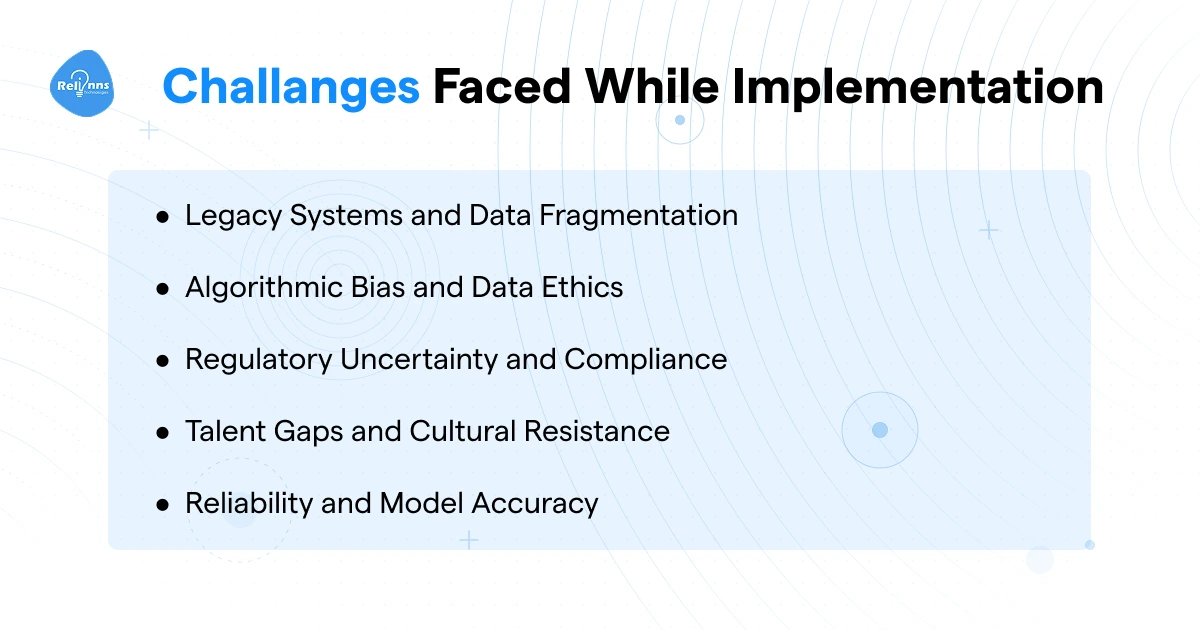

Challenges Faced during AI Adoption in Life Insurance

I'll be straight with you: AI in life insurance doesn't slot in cleanly. There are real friction points, and pretending otherwise doesn't help anyone making a serious decision.

1. Legacy Systems and Data Fragmentation

Most carriers are sitting on infrastructure that wasn't built to talk to modern AI tools. Data lives in silos. Formats don't match across departments. And migrating out of that is expensive, slow, and needs leadership commitment from the top, not just the IT team.

2. Algorithmic Bias and Data Ethics

Models trained on historical data inherit historical patterns, including the unfair ones. If past underwriting decisions carried demographic bias, a model trained on that data will replicate it. This isn't a theoretical risk, it's a regulatory and reputational one. Continuous auditing isn't optional.

3. Regulatory Uncertainty and Compliance

The rules around artificial intelligence in life insurance vary by market and they're still being written. The NAIC 2023 Model Bulletin set a baseline in the US, but it doesn't cover everything, and it doesn't translate to UAE or Saudi regulatory frameworks. Explainability requirements differ. Auditability standards differ. You need legal and compliance in the room from day one.

4. Talent Gaps and Cultural Resistance

Finding people who understand both AI and insurance is genuinely hard. What's just as hard is getting existing teams to trust the tools. Employees who fear displacement disengage, and an AI rollout that the team works around is worse than no rollout at all. Change management matters as much as the technology.

5. Reliability and Model Accuracy

The output is only as good as the data going in. Bad training data produces confident, wrong answers. In underwriting or claims, a confident wrong answer is costly. Human review stays necessary, especially on edge cases. The future of life insurance industry won't be fully automated, and anyone selling you that picture is overselling.

Specific Applications of AI in Life Insurance

This is where it gets concrete. Not what AI could theoretically do, but what it's actually doing inside carriers right now.

1. Automated Underwriting and Risk Assessment

Machine learning models pull in health history, prescription data, and behavioral signals, then classify applicants into risk tiers and recommend pricing in real time. Gradient boosting and neural networks do the heavy lifting. Ethos Life took this far enough to remove the medical exam entirely for many applicants, cutting approval time from weeks to minutes while expanding access to previously underserved segments.

2. Policy Lapse Prediction and Retention

Zurich Insurance runs lapse prediction models that analyze payment history, digital activity, and customer behavior to flag accounts before they go cold. The system feeds alerts directly into CRM, triggering retention outreach before the policyholder has made any decision to leave. Catching a lapse before it happens is significantly cheaper than trying to win the customer back after.

3. Claims Fraud Detection and Prevention

Random forest models and unsupervised clustering compare incoming claims against known fraud patterns and surface inconsistencies across death certificates, financial transactions, and application history. One carrier deploying this approach flagged over 200 high-risk claims within weeks of going live, recovering millions in prevented losses. The speed advantage alone justifies the investment.

4. Personalized Customer Engagement

Insurance AI agents powered by NLP analyze support transcripts and policyholder profiles to trigger the right communication at the right moment. Lemonade's AI assistant Maya handles the full journey from quote to claim without human involvement, and it does it at a scale no human team could match. Artificial intelligence in life insurance at this level means personalization stops being a marketing aspiration and starts being an operational reality.

5. Synthetic Data for Model Training

Privacy laws and data scarcity slow AI development in regulated industries. Generative adversarial networks (GANs) solve this by creating realistic but entirely fictitious policyholder and claim records that carry the same statistical properties as real data. Models get trained faster, tested more thoroughly, and deployed without compliance exposure. McKinsey has flagged this as a key accelerator for AI in life insurance, particularly in markets with strict data handling requirements.

6. Dynamic Pricing and Real-Time Risk Adjustment

Wearable devices and IoT data feed continuous risk recalibration, letting premiums adjust based on live health indicators rather than a point-in-time snapshot. Earnix and Akur8 are the platforms making this scalable and auditable. One carrier using Earnix's dynamic pricing engine saw a 15% increase in quote-to-bind conversion rates by offering pricing that actually reflected individual risk in the moment.

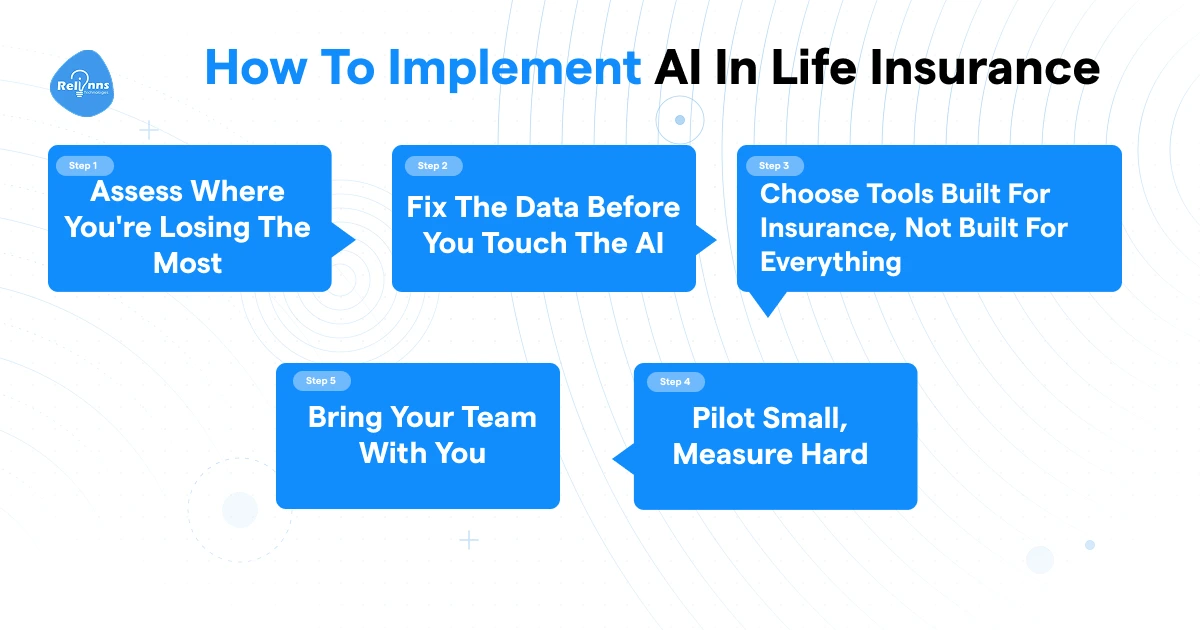

How to Implement AI in Life Insurance

Most failed AI rollouts don't fail because the technology didn't work. They fail because the organization wasn't ready for it. Here's how to do this in an order that actually holds.

Step 1: Assess Where You're Losing the Most

Start with the friction, not the technology. Where does your team spend hours on work that shouldn't need hours? Underwriting backlogs, high lapse rates, fraud slipping through, agents buried in admin. Pick the highest-cost problem and start there. Also check your tech stack honestly. If your core systems can't connect to an API or push data to a cloud environment, that's the first wall you'll hit.

Step 2: Fix the Data Before You Touch the AI

This is the step most teams skip, and it's the reason pilots stall. AI in life insurance runs on clean, centralized data. If your policyholder records are fragmented across departments with inconsistent formats, your model will learn from noise. SulAmérica cleaned over 20% of duplicate entries from a 21 million-record database before their AI programs produced reliable results. Clean data isn't a nice-to-have. It's the prerequisite.

Step 3: Choose Tools Built for Insurance, Not Built for Everything

Generic AI platforms weren't trained on policy structures, claim workflows, or underwriting logic. Artificial intelligence in life insurance performs better on vertical-specific tools. Evaluate vendors on three things: how well their outputs can be explained to a regulator, how cleanly they integrate with your existing systems, and whether they understand compliance requirements in your market. Evident's AI Insurance Index is a useful benchmarking resource here.

Step 4: Pilot Small, Measure Hard

Pick one contained use case. Automated underwriting for straightforward applications. An insurance AI agent handling policy FAQ queries. Run it for 60 to 90 days and track specific numbers: processing time, fraud flag rate, lapse reduction, or customer satisfaction scores. Don't scale until the pilot numbers give you something real to stand behind.

Step 5: Bring Your Team With You

The AI for life insurance agent rollout that the team works around is worse than no rollout at all. Train staff on what the tools do well and where human judgment still leads. Build collaboration between actuarial, IT, compliance, and customer service from the start. Frame AI as something that takes the repetitive work off their plate, not something that's coming for their jobs.

Real-World Examples of AI in Life Insurance

Numbers are useful. Seeing what another carrier actually built is more useful.

Lemonade: Claims in 3 Seconds

Lemonade's problem was straightforward: slow, manual claims processing with high overhead and a digital experience that didn't match what their customer base expected. Their solution was to automate the full claims journey. Maya, their AI chatbot, handles onboarding and customer queries. Backend ML models process, review, and approve claims without human involvement for eligible cases.

The result: claims approved in as little as 3 seconds. Fraud risk dropped because the models catch inconsistencies faster than manual review ever could. And the whole operation scaled to term life coverage without the cost base growing alongside it. That's what AI in life insurance looks like when it's built into the product, not bolted onto the side.

ZhongAn: Pricing That Moves With the Market

ZhongAn is China's first fully digital insurer, and their challenge was scale. Millions of applications, a competitive market, and traditional actuarial methods that couldn't keep up with real-time customer behavior.

Their AI models continuously analyze transactional data, customer behavior, and environmental signals, adjusting pricing dynamically as conditions change. The outcome: millions of applications processed daily with millisecond-level pricing decisions. Profitability improved because the risk-reward calibration got sharper. Insurance AI agents and pricing models working together at that speed isn't a future state for ZhongAn. It's how they run today.

Both cases point to the same thing. Artificial intelligence in life insurance compounds fastest when it's embedded in core operations, not tested at the edges.

Can Insurance Agents Trust AI?

Short answer: yes, with conditions.

AI in life insurance is improving fast, but it still gets things wrong. Generative AI tools hallucinate. They return confident, specific, completely false information without flagging it. That's not a rare edge case, it's a known limitation of how these models work.

Output quality depends entirely on how the tool was built and what data it was trained on. A poorly trained model gives you bad answers at scale.

Never put confidential client information or personal data into free or unvetted AI tools. Free tiers of tools like ChatGPT may use your inputs to train future models, and they carry real data breach risk. The right posture for any AI for life insurance agent: treat every output as a first draft that needs a human to review before it goes anywhere near a client.

Compliance Guardrails: What AI Can and Cannot Do

AI handles the automation. You remain legally responsible for suitability, recommendations, and advice. That line doesn't move.

Review every AI output before acting on it or sending it to a client. On the operational side, recording consent laws vary. Federal law requires one-party consent. Many states require all parties to agree before a call is recorded. Verify the rules in both your state and your client's state before any AI tool touches a conversation.

Automated outbound SMS and calling fall under TCPA regulations. Always include opt-out options. Insurance AI agents that skip this step create legal exposure fast.

How to Start Without Disrupting What Is Working

The agents who struggle most with AI try to overhaul everything at once. That's how you get a half-working system that the team works around.

Start with one gap. Set up a 5-touch automated follow-up sequence for new leads and run it for 30 days. Track response rates and close rates. Don't touch anything else until those numbers stabilize.

Then add discovery capture. Bring in an AI assistant for your calls, give it 30 days, and watch what happens to proposal quality and clean submission rates.

Post-meeting execution comes last, once the follow-up and capture workflows are solid. Automated CRM sync, follow-up drafting, form-fills. Build on what's working, not on what looks impressive on a demo.

What the AI-First Insurer Looks Like

AI-first insurers don't organize around internal departments. They organize around customer journeys, with shared data and AI-driven workflows connecting underwriting, servicing, sales, product development, and investment management into one coherent system.

The practical result: straight-through decisions become standard for most applications. Simple claims get approved and paid in minutes. The insurer stops being just a risk manager and starts being something closer to a financial partner.

BCG maps this across three moves: Deploy (near-term productivity gains), Reshape (core workflow redesign), and Invent (new business models built on connected data). Carriers leading on this track show 60% faster annual revenue growth and 30% higher three-year growth than laggards. Artificial intelligence in life insurance at scale isn't an IT project. It's a business model shift.

The Future of Life Insurance

The one-and-done application is going away. The future of life insurance industry runs on continuous data, wearables, electronic health records, and social determinants of health feeding real-time underwriting models that update policy terms as customers' lives change.

Generative AI will let agents and LLMs co-create policy documents tailored to individual profiles in seconds. Computer vision may handle remote medical assessments, making fully virtual onboarding and claims processing standard rather than exceptional.

The carriers building interoperable data infrastructure and cross-functional AI capabilities today will have a structural lead by 2030. The ones waiting for a cleaner moment to start will be catching up to competitors who've already moved. AI in life insurance rewards early movers and compounds over time.

Final Word

The gap between carriers using AI well and those still evaluating it is already showing up in revenue growth, conversion rates, and retention numbers. This isn't a future problem.

AI in life insurance has moved from experiment to operational reality. The window to build an early advantage is open, but it won't stay open indefinitely.

If you're ready to move from evaluation to implementation, Relinns builds insurance-specific AI solutions, from voice agents and chatbots to full insurance platform development with AI embedded from the ground up. Talk to our team and let's figure out where AI moves the needle fastest for your business.

Frequently Asked Questions (FAQs)

Will AI replace insurance agents?

No. Repetitive, data-intensive tasks are automatable. Trust, judgment, and relationship management are not. Agencies using AI to remove admin work from their agents see better client outcomes, not smaller teams.

How will AI affect insurance agents?

The immediate effect is time. AI for life insurance agents clears administrative overhead and frees capacity for higher-value work. The longer-term effect is competitive positioning. Agencies building AI into workflows now will handle more accounts without adding headcount or burning out their teams.

How is AI commonly used in the insurance industry?

Underwriting automation, claims processing, fraud detection, policy lapse prediction, customer engagement personalization, and dynamic pricing are the most common active deployments of artificial intelligence in life insurance today.

What AI tools are insurance agents actually using?

CRM automation through AgencyZoom, HubSpot, and Salesforce Financial Services Cloud. AI meeting assistants like Zocks for discovery capture. Document tools like Docusign Iris and Snapsheet. Content generation via ChatGPT and Jasper. Lead scoring through Planck AI and Salesforce Einstein.

Is it legal to use AI to record client meetings?

Federal law requires one-party consent. Many states require all parties to agree. Verify requirements in both your state and your client's state before any insurance AI agents or recording tools touch a conversation.

Sources:

https://www.salesforce.com/financial-services/artificial-intelligence/ai-for-insurance-agents/

https://www.bcg.com/publications/2026/the-ai-first-life-insurance-company