Types of Low Code Digital Onboarding Solutions for Banks

Date

Aug 04, 25

Reading Time

11 Minutes

Category

Low-Code/No-Code Development

Share

Introduction

Banks are under increasing pressure to streamline customer acquisition.

Digital onboarding – the online process where new users verify identity and open accounts without in-person visits – has become essential. 78% of US consumers now prefer to do their banking digitally. (Source: MoneyZine)

At the same time, low-code development is transforming banking IT: the global low-code market is growing rapidly (from $22.5B in 2022 to $32B in 2024), and one study projects that by 2029, 80% of new mission-critical banking apps will be built on low-code platforms.

This post explores seven key low-code digital onboarding solutions for banks (like eKYC, video KYC, biometrics, OCR document checks, mobile apps, chatbots, and ID verification) and explains how each addresses onboarding challenges.

We’ll also cover how low-code makes compliance easier, how to choose the right onboarding flow, and what the future holds for digital onboarding solutions for banks.

In short, implementing modern digital onboarding solutions for banks means faster sign-ups and stronger compliance.

The Trouble with Traditional Onboarding

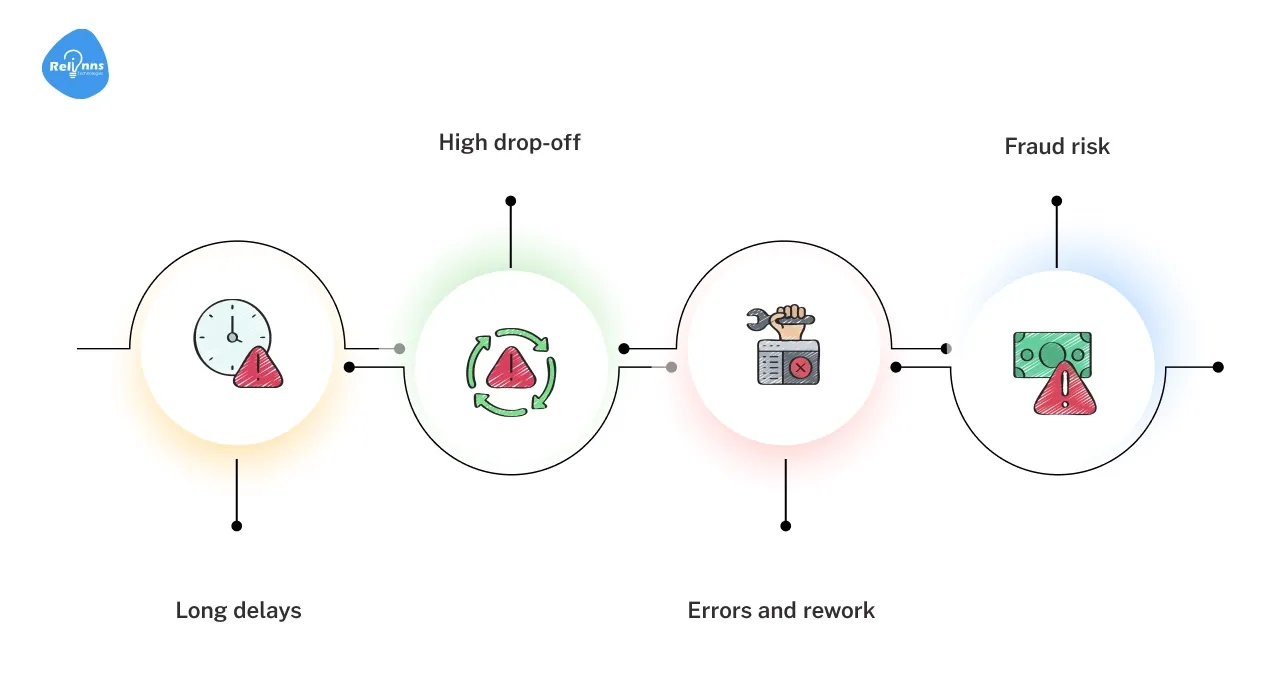

Traditional onboarding in banking is often a slow, fragmented experience that frustrates customers and staff alike. Manual forms, outdated systems, and compliance hurdles create delays that drive users away before they even open an account.

- Long delays: 67% of banks say they have lost customers due to slow, manual onboarding processes.

- High drop-off: Nearly half of consumers who encounter friction switch banks, and 68% abandon online applications if steps are too lengthy.

- Errors and rework: Cumbersome forms lead to mistakes. Customer abandonment can exceed 50% if onboarding takes more than a few minutes.

- Fraud risk: Outdated manual checks make banks vulnerable – new-account fraud jumped 109% in 2021.

These problems – delays, errors, poor user experience, and fraud – show why legacy onboarding must be replaced by efficient digital onboarding solutions for banks.

What Low-Code Brings to Digital Onboarding Solutions for Banks

Low-code platforms bring dramatic speed and flexibility gains for banks. For example, research shows low-code development can cut app build time by 50–90%, slashing time-to-market for new onboarding features.

Non-technical staff can use visual tools to update workflows quickly, so banks can adjust KYC steps or add identity checks on the fly.

Prebuilt connectors and APIs enable seamless integration with core banking systems, CRM, fraud databases, and identity providers. For banks, this means they can assemble complete digital onboarding solutions for banks much faster.

In fact, Gartner predicts that by 2029, 80% of mission-critical applications will be built on low-code, which will include many new digital onboarding solutions for banks.

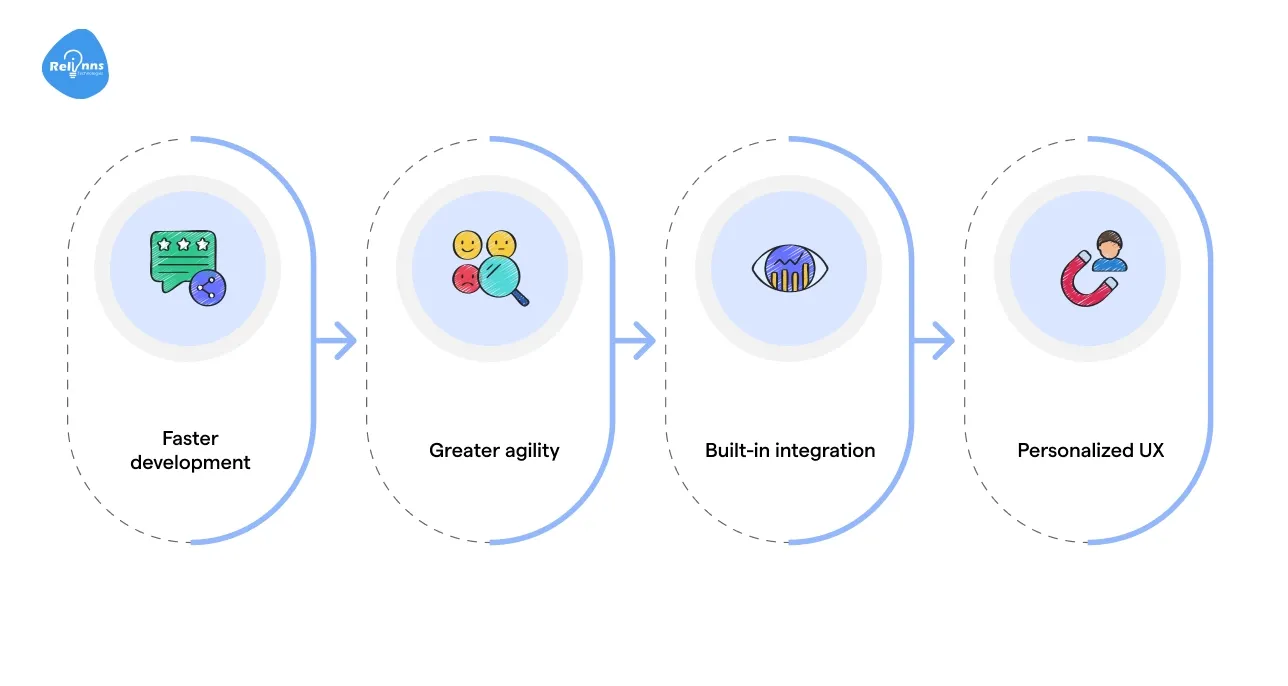

- Faster development: Build and iterate onboarding apps in days, not months – studies report 50–90% reductions in dev time.

- Greater agility: Business teams can tweak forms, workflows, or branding quickly with drag-and-drop tools.

- Built-in integration: Low-code connectors link to core systems and fintech tools, enabling real-time data sharing and checks.

- Personalized UX: Prebuilt analytics and templates let banks tailor the experience on the fly using real-time customer data.

For banks, low-code means they can assemble a full suite of digital onboarding solutions for banks far faster than with traditional coding.

7 Types of Low-Code Digital Onboarding Solutions for Banks

Banks today need onboarding systems that are fast, secure, and adaptable to diverse customer needs. Low-code platforms enable the mixing and matching of onboarding components based on use case, geography, and risk profile.

Below, we detail seven key low-code digital onboarding solutions for banks that can transform customer acquisition.

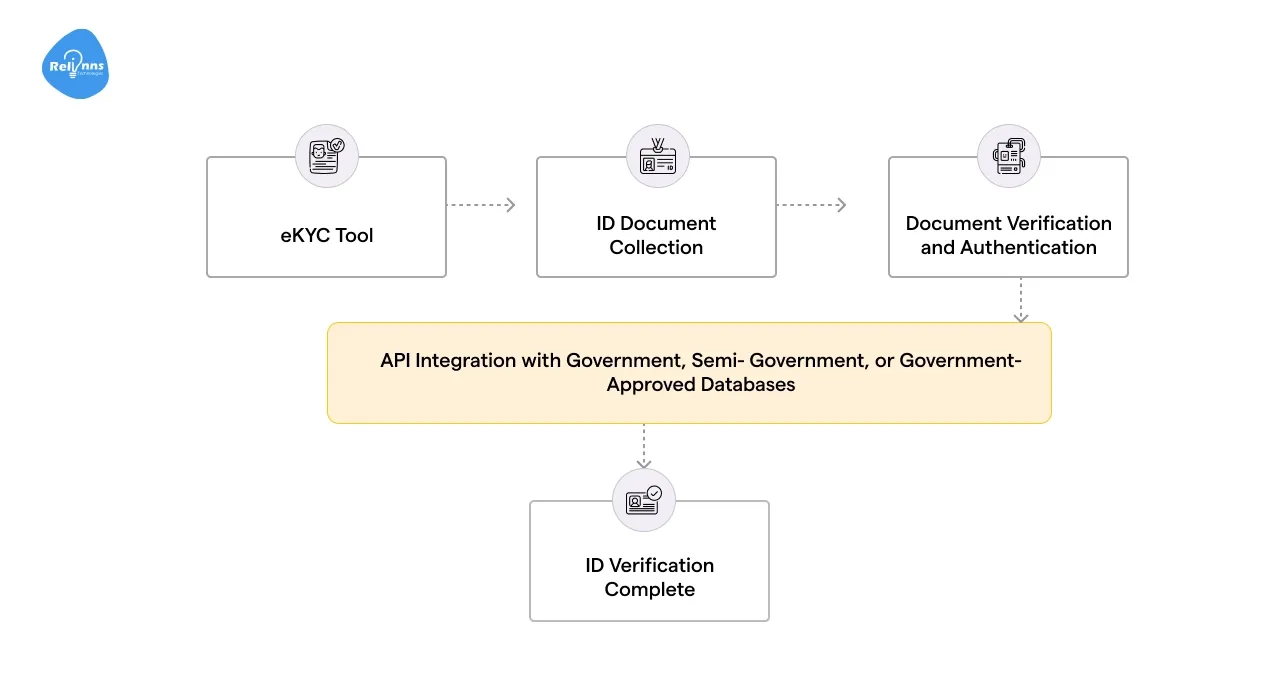

1. eKYC Modules

Electronic Know-Your-Customer (eKYC) modules automate identity verification by linking to authoritative ID sources (like government registries or credit bureaus).

In practice, a user’s photo of a passport or driver’s license is instantly checked against official data, and liveness is verified. This greatly reduces manual processing.

For example, one McKinsey noted eKYC can cut onboarding times by up to 90%. eKYC is also a fast-growing market (projected to reach $2.79B by 2030) as regulators worldwide push for digital ID checks.

In short, eKYC modules are a core part of modern digital onboarding solutions for banks, streamlining KYC while meeting compliance.

2. Video KYC with Agent Assist

Video KYC uses a live video call to verify a customer’s ID. The customer shows their ID to the camera, and a remote agent (often aided by AI) confirms the details and facial liveness.

This hybrid human-AI approach satisfies strict regulations (for example, RBI’s V-CIP in India or upcoming EU AML rules recognize video KYC).

Video KYC is becoming mainstream: the market was about $0.29B in 2024 and may exceed $1.03B by 2033. Banks like this method – one fintech found 25–30% more completed sign-ups when using live video versus static uploads. (Source: BusinessResearchInsights)

Video KYC is one example of a low-code digital onboarding solution for banks that boosts trust and conversion.

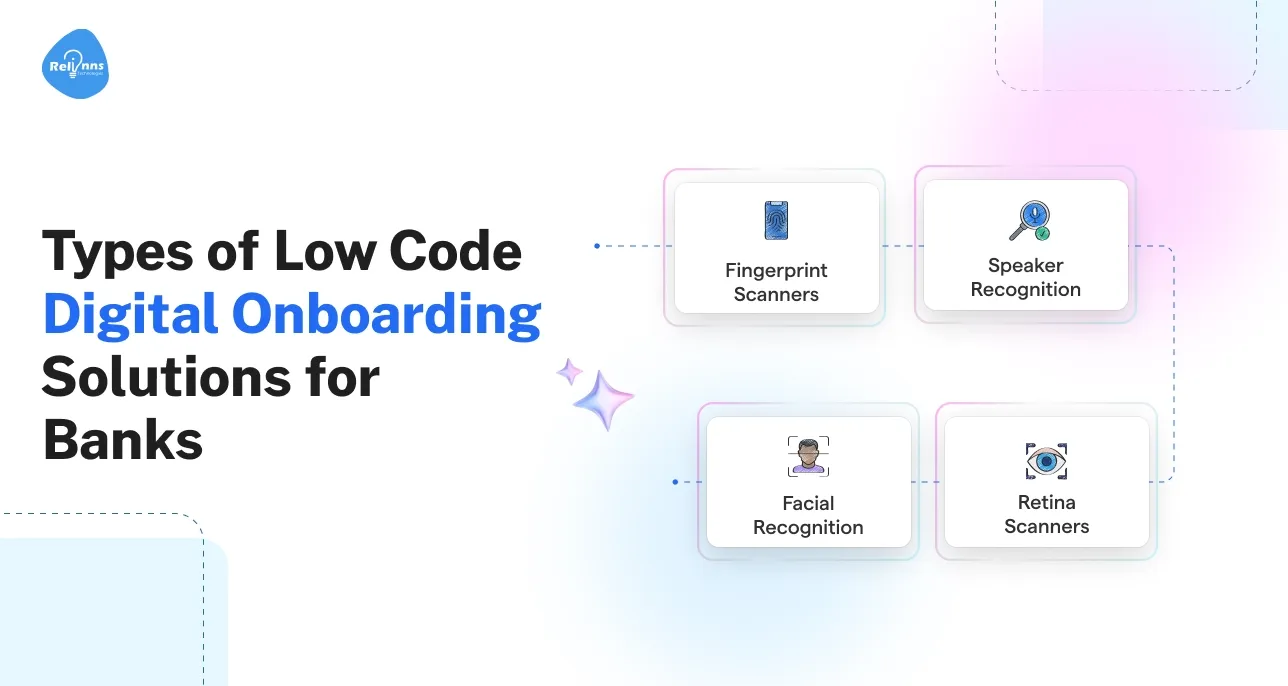

3. Biometric Authentication

Modern onboarding often uses biometrics (fingerprint, face recognition, iris, or voice). According to industry research, 83% of banks worldwide now deploy at least one biometric method in their services.

Adding biometrics in onboarding is easy with low-code modules: a mobile app can prompt a fingerprint scan or selfie and match it to the ID on file instantly.

This not only speeds the process (no typing IDs) but greatly reduces fraud. In fact, KPMG found banks saw a 66% reduction in account takeover fraud within a year of multi-modal biometric adoption.

Biometrics form a key element of most low-code digital onboarding solutions for banks, providing security and convenience.

4. Document Upload with OCR & AI Matching

Low-code onboarding solutions often include smart document handlers.

Customers simply take a photo of a document (ID, passport, utility bill, etc.) and the system uses Optical Character Recognition (OCR) and AI to extract and verify the data. This eliminates manual data entry and errors.

Advanced AI can flag tampered documents or match names across forms. Banks using AI for KYC report dramatic savings – for example, AI-driven flows can reduce costs by 30–40%. (Source: Datavisor)

OCR and AI modules are powerful features in digital onboarding solutions for banks, auto-filling forms and detecting fraud instantly.

5. App-Based Mobile Onboarding

Given how many people bank on phones, mobile-first onboarding is critical. Recent data shows 68% of U.S. consumers manage their accounts via a mobile banking app (45% use such apps daily).

For banks, this means onboarding must work flawlessly on mobile. Low-code mobile onboarding solutions enable users to register in the bank’s app through steps such as document scanning, selfie capture, and one-time passwords.

Push notifications and device sensors (GPS, device ID) can enhance fraud checks.

In practice, a seamless in-app flow is now standard in many digital onboarding solutions for banks, meeting customers where they are and reducing drop-offs.

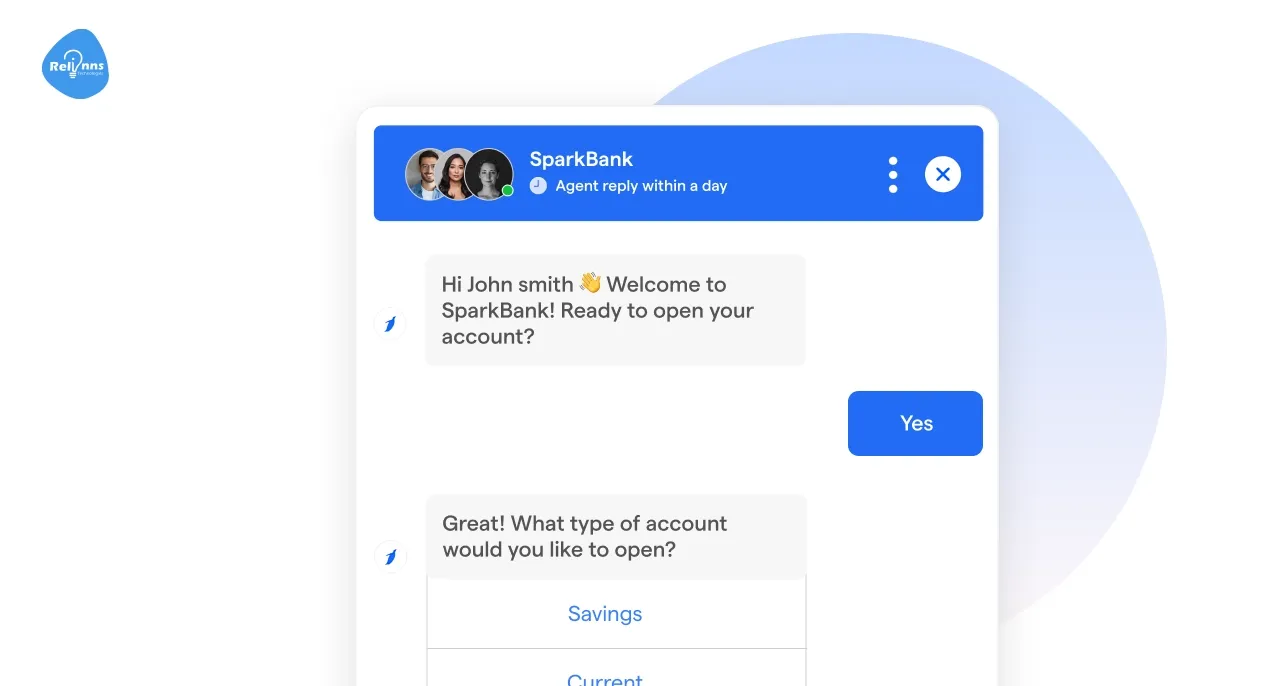

6. Chatbot-Driven Journeys

Chatbots and virtual assistants can guide customers through onboarding in a conversational way. Instead of static forms, the user answers step-by-step questions in a chat interface.

Chatbots can dynamically ask for documents, send verification codes, and flag any errors.

This approach boosts engagement: about 68% of consumers have used a customer-service chatbot, and usage is even higher among younger users (72% of under-40s).

Low-code platforms often include chatbot builders, allowing banks to script guided dialogues quickly. Chatbot flows are now a staple of many digital onboarding solutions for banks, providing a personalized, 24/7 onboarding experience.

7. Utility and Social ID Verification

For extra trust, some onboarding solutions verify identity using utility and social data. This could mean confirming an address from an electricity bill or matching a user’s tax ID (Social Security Number) with government records.

Some platforms even allow “social login” (sign in with Google/Facebook) as proof of identity. These checks supplement standard KYC.

Low-code onboarding solutions can incorporate prebuilt checks: for example, the app might request a utility bill photo (with OCR) or send an SMS to a verified phone number.

Together with the other modules, these steps complete a robust set of digital onboarding solutions for banks.

Compliance Made Easy with Digital Onboarding Solutions for Banks

Low-code doesn’t just speed development; it embeds compliance controls into the process. Low-code platforms include standard modules for KYC/AML rules, so regulators’ requirements are part of the workflow by default.

For example, built-in rules enforce ID checks, document retention, and audit logging. When regulations change (new AML directives, PSD2, CCPA, etc.), banks can modify the onboarding flow via configuration – no recoding entire systems.

Low-code apps often feature automatic logging of each step.

This agility makes low-code platforms the backbone of flexible digital onboarding solutions for banks that stay up-to-date with regulations.

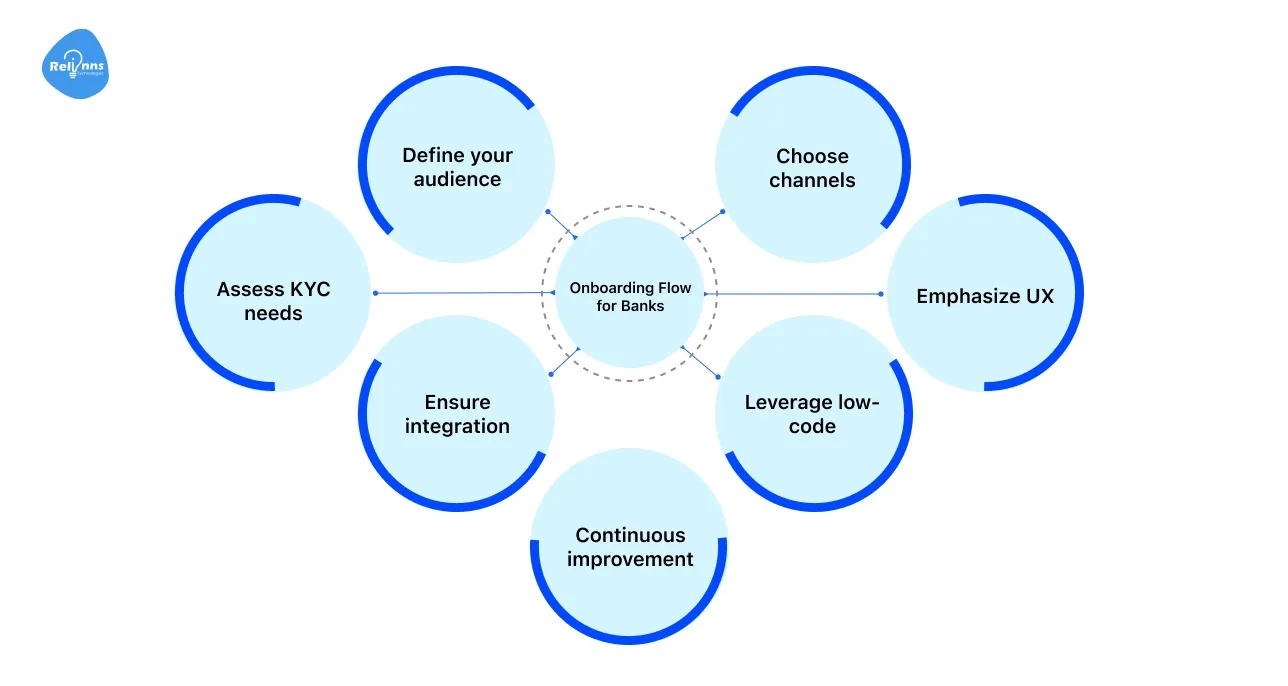

How to Pick the Right Onboarding Flow for Banks

Effective onboarding is crucial for ensuring a smooth customer experience while maintaining strong security standards. Since customers come with different needs and risk levels, banks must adopt flexible onboarding methods that balance convenience with compliance.

Banks should tailor their onboarding approach to their customers and risk profile.

- Define your audience: Are they retail customers or corporate clients? Younger demographics may demand fully digital flows, while others might need a hybrid approach.

- Choose channels: Decide if you’ll use mobile app, web portal, video call, or chat. For a mobile-first audience, a smooth in-app experience is essential.

- Assess KYC needs: Determine required identity checks (basic eKYC vs enhanced due diligence). Combine elements (ID scans, selfies, fraud screening) as needed.

- Emphasize UX: Keep each step clear and necessary. Use progressive disclosure (ask only essential info first) to reduce drop-offs.

- Ensure integration: Verify that the solution connects to your core banking, CRM, fraud engines, and provides dashboards.

- Leverage low-code: Choose a platform you can adapt easily (adding fields, changing workflow, localizing) without heavy coding.

- Continuous improvement: A/B test flows to refine your digital onboarding solutions for banks based on user metrics.

Ultimately, the “right” flow balances regulatory compliance with user convenience.

In practice, banks using a flexible low-code platform can experiment with multiple digital onboarding solutions for banks in parallel and optimize continuously, keeping the best features and discarding the rest.

What’s Next: Future-Ready Digital Onboarding Solutions for Banks

The future of onboarding is AI-driven, omnichannel, and hyper-personalized. AI/ML tools will increasingly auto-validate documents, flag suspicious patterns, and personalize offers during signup.

In fact, 72% of banking customers agree that AI will soon deliver easy, convenient self-service. (Source: JD Power)

For example, generative AI may power intelligent chat assistants that not only verify identity but also recommend products.

Voice KYC and behavioral biometrics will augment existing checks. Decentralized ID (digital wallets) and blockchain credentials are emerging globally.

As these trends unfold, leading digital onboarding solutions for banks will seamlessly integrate AI, machine learning, and new identity schemes, allowing banks to adjust instantly to new technologies.

Final Takeaways on Digital Onboarding Solutions for Banks

Modern onboarding demands agility. Traditional methods are slow, error-prone, and unsafe – a recipe for lost customers.

Low-code solutions change the game by letting banks deploy robust, innovative onboarding systems fast.

In this post, we covered seven key digital onboarding solutions for banks: eKYC modules, video KYC, biometric auth, OCR/AI document checks, mobile app flows, chatbots, and utility/social verification.

Each addresses a facet of the challenge (speed, accuracy, fraud prevention, or UX). Together, they form a comprehensive onboarding toolkit.

The bottom line: banks that invest in low-code digital onboarding solutions for banks see real impact, and robust digital onboarding solutions for banks are no longer optional – they are critical for growth and customer trust.

Why Choose Relinns Technologies for Digital Onboarding Solutions for Banks?

Relinns Technologies delivers a flexible low-code/no-code platform powered by Joget, enabling banks to build custom digital onboarding workflows quickly and efficiently.

- 8+ years of experience: Packing nearly a decade of experience in 35+ industries.

- 50–90% faster development: Low-code/no-code accelerates workflow without coding.

- Mobile friendly: Enables onboarding accessible on any device, anytime, anywhere.

- Flexible integration: Connects easily with banking systems and third-party tools.

- 70% More Cost-effective: Automates data verification to reduce operational expenses.

- Improved conversions: Customizable flows boost customer onboarding success rates.

We empower banks with a customizable platform to build digital onboarding solutions that fit unique business needs. Ready to modernize your onboarding and accelerate customer acquisition?

Frequently Asked Questions (FAQs)

How does a low-code platform improve compliance in digital onboarding solutions?

Low-code platforms simplify regulatory compliance by enabling quick updates to workflows, integrating compliance checks, and reducing human error, ensuring banks meet evolving legal requirements without extensive IT resources or delays.

What role does AI play in enhancing security during customer onboarding?

AI enhances onboarding security by detecting fraud patterns, verifying identities through advanced biometrics, and automating risk assessments, providing faster, more accurate verification while reducing manual workload and errors.

Can biometric security solutions adapt to different customer preferences in banking?

Yes, biometric systems support multiple modalities such as fingerprint, facial, and voice recognition, allowing banks to offer flexible, user-friendly authentication options tailored to diverse customer needs and device capabilities.

How does mobile-first onboarding impact customer acquisition and retention?

Mobile-first onboarding meets customers where they engage most, enabling quick, convenient access on smartphones. This approach improves satisfaction, accelerates account openings, and increases long-term loyalty by reducing friction in onboarding.

What are the scalability advantages of using a low-code platform for bank onboarding?

Low-code platforms enable banks to scale onboarding operations efficiently by rapidly deploying new features, integrating with multiple systems, and easily adapting to growing user bases without significant development overhead.

How do multi-factor authentication and video KYC together reduce fraud risks?

Combining multi-factor authentication with video KYC creates layered security, verifying identity through multiple channels, deterring fraud attempts, and ensuring thorough customer verification beyond traditional document checks.