A Complete Guide to Digital Onboarding in Banking Using Low Code

Date

Jul 31, 25

Reading Time

23 Minutes

Category

Low-Code/No-Code Development

Share

Digital onboarding in banking is now essential as customers expect quick, paperless account openings without visiting a branch. Meeting these expectations while staying compliant can be difficult for many institutions.

Traditional development makes changes slow and expensive, often creating delays that frustrate customers and increase costs.

Digital onboarding in banking using low code solves this challenge by enabling faster workflow design, easier updates, and a smoother customer journey. This guide explains how banks can put it into practice.

What Is Digital Onboarding in Banking and How Low-Code Simplifies It?

Digital onboarding in banking refers to the end-to-end process of acquiring, verifying, and activating new customers through digital channels, eliminating the need for physical presence or paperwork.

This technology-driven approach transforms the traditionally cumbersome customer acquisition process into a seamless digital experience.

Increasingly, banks are leveraging low-code platforms to build and deploy these onboarding workflows quickly, without relying on extensive developer resources.

- Digital onboarding enables banks to verify and activate customers entirely online.

- No physical visits are required—everything happens via web or mobile channels.

- KYC verification is done through selfie capture and ID document scanning.

- Users input their personal information and digitally sign all necessary agreements.

- Account activation is completed in minutes, offering instant access to services.

- Real example: ICICI Bank allows new users to onboard entirely via its mobile app.

- Result: A fully functional bank account without paperwork or branch visits.

Low-code tools simplify the creation and modification of these steps, allowing banks to adapt onboarding flows to new compliance rules or user feedback without heavy redevelopment cycles.

Real example: ICICI Bank allows new users to onboard entirely via its mobile app.

Result: A fully functional bank account without paperwork or branch visits.

How Digital Onboarding in Banking Works with Low-Code Platforms

Digital onboarding in banking follows a systematic approach designed to verify identity, assess risk, and establish a customer relationship completely through digital means.

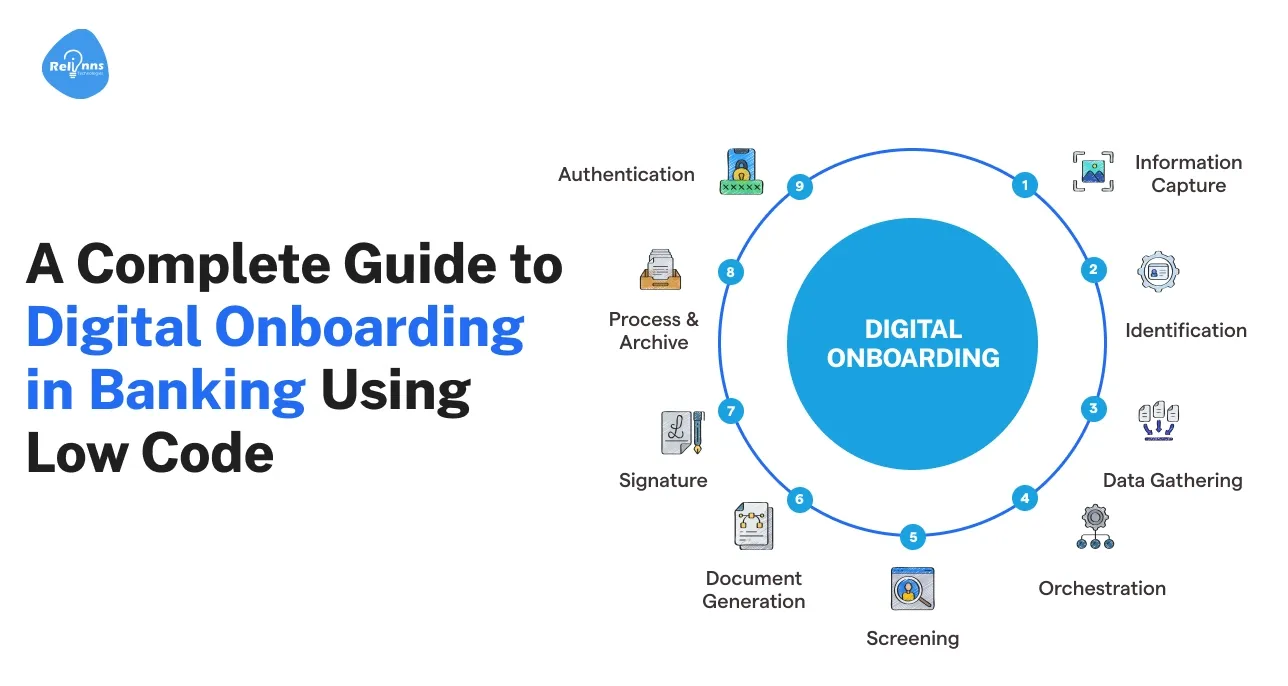

1. The Digital Onboarding Process: Step-by-Step and Low-Code Enabled

The digital customer onboarding banking process is a streamlined, fully online journey that guides users through identity verification, compliance checks, and account setup, efficiently replacing traditional, paper-heavy methods.

Today, many banks accelerate this process using low-code no-code app development that allow them to build, modify, and optimize these digital flows without heavy backend development.

- Application Initiation: Customers begin by accessing the bank's website or mobile app and selecting the product for which they wish to apply.

- Identity Verification: Includes document capture (e.g., ID cards, passports), biometric verification (face match, fingerprints), and liveness detection to prevent spoofing or fraud.

- Know Your Customer (KYC) Checks: Banks perform instant, automated checks against global watchlists, sanctions databases, and lists of politically exposed persons (PEPs), often completing verifications in seconds.

- Risk Assessment: AI-driven algorithms evaluate applicant data and external sources to assess creditworthiness and fraud risk in real time.

- Digital Signatures: Customers review and sign agreements electronically—today, 65% of banking documents are signed digitally.

- Account Activation: Once verification is successful, the bank instantly activates the account and provides digital credentials for immediate access.

2. Integration Architecture: Connecting Systems Using Low-Code Middleware

Behind the scenes, digital onboarding in banking relies on sophisticated technology integration. The user-facing channels (mobile apps and websites) connect to middleware platforms that orchestrate the verification process.

Low-code integration layers make this orchestration significantly faster and more adaptable by providing pre-built connectors and visual API tools.

These platforms interact with the following.

- Core banking systems

- Third-party verification services

- Regulatory compliance engines

- Document management systems

- Customer relationship management (CRM) tools

Many insurers—especially in personal lines—automatically approve approximately 75% of applications through STP, reflecting the ability to process a significant majority of cases without human intervention. (Source: InsuranceThoughtLeadership)

Low-code orchestration tools help enable such high levels of automation by reducing the need for custom development when linking new systems or partners. This agility ensures faster deployment of onboarding flows with real-time data exchange.

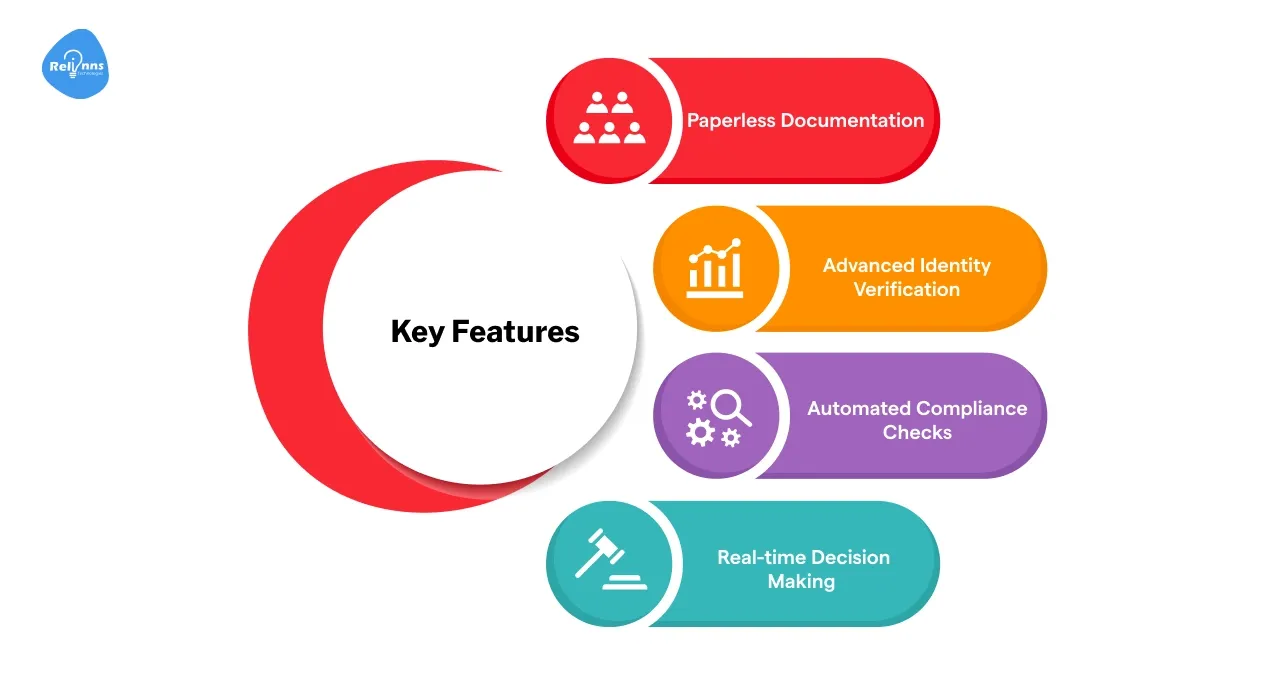

Key Features of Digital Onboarding in Banking Powered by Low-Code

Digital customer onboarding banking platforms come equipped with several essential features that differentiate them from traditional processes. When developed using low-code platforms, these features become faster to implement, easier to modify, and more scalable across banking channels.

Understanding these capabilities helps appreciate the transformative potential of digital onboarding solutions, especially when powered by visual development tools and pre-built integrations.

1. Paperless Documentation

Modern digital onboarding eliminates paper forms by enabling instant data capture, secure digital signatures, and seamless electronic document submission processes.

Low-code platforms make it easy to configure form layouts, e-signature flows, and document automation without coding.

- Digital forms auto-complete fields using previously stored user data.

- Users submit documents electronically, thereby reducing delays.

- Documents are stored securely and retrieved quickly when needed.

- Systems automatically and accurately extract key data from uploaded documents.

Intelligent Document Processing (IDP) reduces processing time by 50% and nearly eliminates errors, dramatically improving efficiency. (Source: Nividous).

2. Advanced Identity Verification

Digital onboarding leverages multiple verification methods like biometrics, OTPs, document scanning, and database checks to ensure secure and compliant identity validation.

Using low-code connectors, banks can integrate biometric APIs, face recognition tools, and OTP services in days, not months.

- AI detects IDs with over 99% accuracy for identity verification.

- Facial recognition uses liveness detection to prevent spoofing attacks.

- Biometric systems include fingerprints and voice for secure authentication.

- One-time password (OTP) ensures multi-factor verification via SMS/email.

Many banks that implement voice biometrics have reduced fraud losses by up to 80%, benefiting from both cost savings and enhanced security. (Source: gnani)

3. Automated Compliance Checks

Digital onboarding systems automate regulatory checks through real-time AML screening, PEP identification, document verification, risk scoring, and algorithms for detecting suspicious activity.

Low-code logic builders and workflow engines allow compliance teams to update rules dynamically without redeploying the entire application.

- Screens identities instantly against AML/CFT watchlists for compliance.

- Flag individuals during PEP checks for enhanced due diligence.

- Utilizes risk scoring algorithms to categorize users based on their potential for fraud.

- Detects suspicious activity patterns to alert compliance teams fast.

Banks implementing AI-driven compliance solutions have seen false positives drop by up to 40% and compliance costs decrease by at least 20%. (Source: IBS Intelligence)

4. Real-time Decision Making

Modern digital onboarding platforms enable instant identity verification, automated compliance checks, seamless form filling, secure document submission, and real-time user status updates.

With low-code rule engines and AI integration, banks can build decision logic that updates in minutes, improving agility in credit approvals and customer engagement.

- Instantly assesses creditworthiness using financial and behavioral data.

- Automates approval workflows to reduce manual decision bottlenecks.

- Recommends products dynamically based on customer profiles and needs.

- Sends real-time application status updates to keep users informed.

According to an analysis by Number Analytics, real-time credit scoring enables instant credit decisions and increases conversion rates by up to 35% for digital applications. (Source: NumberAnalytics)

Top Benefits of Digital Onboarding for Banks and Customers Using Low-Code

Digital onboarding in banking generates substantial value for both financial institutions and their customers, which explains its rapid adoption across the industry.

When powered by low-code platforms, the speed, adaptability, and cost-effectiveness of these benefits are amplified, enabling banks to launch and optimize digital onboarding flows with minimal developer effort.

A. Benefits for Financial Institutions

Digital onboarding in banking enables financial institutions to reduce costs, enhance compliance, accelerate customer acquisition, and improve security through automated verification and real-time identity checks, ultimately boosting overall efficiency and trust.

1. Operational Efficiency

Digital customer onboarding in banking significantly reduces operational costs by automating tasks, minimizing errors, and eliminating the need for manual processing.

Low-code platforms further enhance this by allowing process automation to be implemented without extensive coding.

Key factors

- Cuts physical infrastructure costs significantly for smoother operations

- Minimizes document processing and storage expenses effectively.

- Lowers staff workload by automating identity verification tasks.

- Reduces manual errors, enhancing accuracy in onboarding processes.

- Speeds up customer onboarding, consistently saving time and resources.

2. Higher Conversion Rates

Banks see a 20-40% boost in application completions with digital onboarding, thanks to faster, user-friendly, and more accessible processes.

With low-code customization, banks can quickly optimize UX based on real-time analytics or feedback, eliminating the need for full rebuilds.

Key factors

- Simplified process lowers drop-off rates during onboarding.

- Quicker decisions boost customer engagement and trust.

- Accessible on all devices and from remote locations.

- Users can pause and resume applications at any time, from anywhere.

- Enhanced UX drives higher conversion and satisfaction rates.

3. Improved Data Quality

Digital onboarding systems capture customer data with greater accuracy and structure, enabling more informed decision-making and personalized experiences.

Low-code integrations standardize data across systems, reducing inconsistencies and enabling real-time syncing with CRMs and analytics platforms.

Key factors

- Automated validation reduces input errors by up to 80%.

- Structured formats improve data analysis and compliance readiness.

- Fewer manual inputs reduce inconsistencies in customer records.

- Centralized data storage simplifies customer information management.

- Richer profiles allow for targeted products and messaging.

B. Benefits for Customers

Digital onboarding offers customers a seamless and convenient experience, featuring faster approvals, secure identity verification, and the flexibility to open accounts anytime, anywhere, without the need to visit a branch.

Low-code-driven platforms ensure these journeys are responsive, personalized, and continuously improved.

1. Time Savings

Digital onboarding in banking reduces customer time investment from days to minutes, offering faster access to services without physical visits or delays.

Low-code platforms empower banks to roll out faster user flows and automate backend processes for real-time results.

Key factors

- 90% less time spent than traditional branch onboarding.

- No need to travel to physical bank branches.

- Eliminates waiting for in-person appointments entirely.

- Immediate access to basic banking features and tools.

- A rapid, hassle-free process greatly enhances the customer experience.

2. Convenience and Accessibility

Digital processes offer unmatched flexibility, enabling users to onboard at any time, from any device or location, with easy-to-use, intuitive platforms.

With low-code tools, banks can quickly create adaptive interfaces that work across devices and geographies.

Key factors

- 24/7 application access enhances user control and freedom.

- Compatible with mobile devices, tablets, and desktops.

- Location-independent process supports remote onboarding.

- User-friendly interface ensures smooth customer navigation.

- Removes the need for in-branch appointments or visits.

3. Enhanced Transparency

Digital onboarding keeps customers informed with clear updates, instant feedback, and complete visibility into their application process and requirements.

Low-code workflows enable real-time alerts, progress tracking, and automated notifications without manual intervention.

Key factors

- Provides real-time status updates at each step.

- Immediate alerts if more information is needed.

- Shows estimated timelines for account activation.

- Customers get digital records of submitted data.

- 86% report higher satisfaction due to transparent tracking.

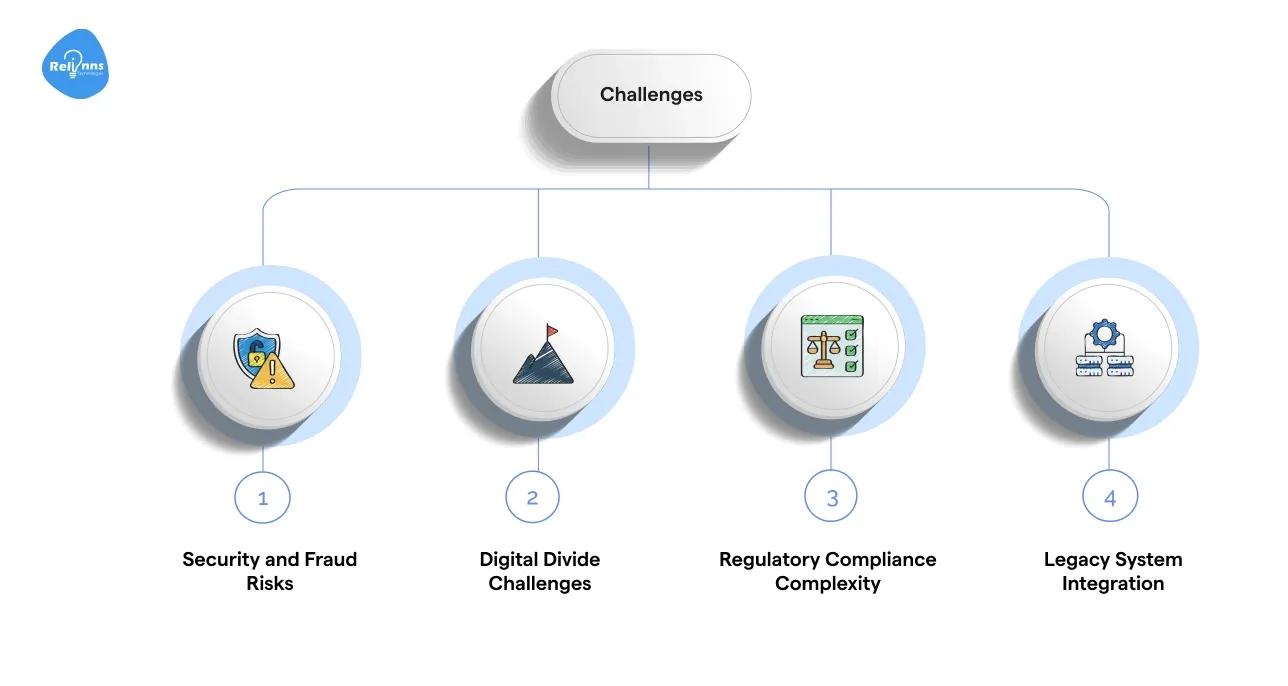

Challenges in Digital Onboarding for Banks and Customers and How Low-Code Solves Them

Despite its many advantages, digital onboarding in banking faces several notable challenges that financial institutions must address to ensure successful implementation.

These hurdles range from fraud risks to legacy tech constraints. Still, when paired with low-code platforms, many of these can be mitigated through rapid iteration, modular integrations, and continuous compliance adaptation.

1. Security and Fraud Risks

With the shift to digital banking, fraud threats have escalated, posing serious challenges to secure and trustworthy onboarding processes.

Key factors

- 43% rise in identity theft during digital onboarding (2021).

- Synthetic identity fraud is now the fastest-growing form of identity theft.

- Advanced document forgery complicates verification efforts.

- Social engineering targets users who are less tech-savvy or vulnerable.

- Increased fraud risk demands stronger authentication systems.

How Low-Code Helps

Low-code platforms allow quick integration of advanced fraud detection tools, like biometric APIs, liveness detection, and behavioral analytics, without full-stack development.

With prebuilt modules and AI connectors, banks can continuously update and reinforce authentication layers, deploying new countermeasures in days rather than months.

2. Digital Divide Challenges

Not all customers have equal digital access or confidence, creating barriers to inclusive digital onboarding in banking services.

Key factors

- 15% of global users lack reliable internet access.

- Older customers report a 30% lower level of digital confidence.

- Rural areas struggle with connectivity and tech literacy.

- Accessibility issues impact users with disabilities.

- Inclusion strategies are crucial for preventing user exclusion.

How Low-Code Helps

Low-code tools enable the creation of highly responsive, device-agnostic onboarding experiences, including voice-enabled flows, multilingual interfaces, and accessible layouts.

Developers can A/B test and adjust the UX based on user demographics with no-code logic updates, making the platform more inclusive.

3. Regulatory Compliance Complexity

Digital onboarding must comply with varying, often outdated regulations, adding friction to the seamless experiences banks aim to deliver.

Key factors

- Regulations vary across regions and countries.

- Cross-border services face extra compliance challenges.

- Legal frameworks often lag behind the development of new technologies.

- Some requirements complicate smooth user experiences.

- Balancing compliance with convenience remains difficult.

How Low-Code Helps

Compliance teams can use low-code rule engines to adjust onboarding logic in response to shifting regulations without code-level redeployment.

For example, changes to KYC thresholds or data retention policies can be applied via a visual dashboard, reducing time-to-compliance dramatically.

4. Legacy System Integration

Many traditional banks face high costs and complexity in aligning outdated systems with modern digital onboarding tools.

Key factors

- Core systems are often decades old and rigid in nature.

- Integration needs expensive customization and development work.

- Siloed data limits a unified customer experience.

- Lack of APIs hinders real-time system communication.

- Legacy banks spend 60–80% more on transformation.

How Low-Code Helps

Low-code middleware can connect modern onboarding workflows to legacy core banking systems through prebuilt connectors, API gateways, or secure hybrid integrations.

This drastically reduces custom coding needs and enables data synchronization between old and new systems in real time.

Regulatory Requirements in Digital Onboarding for Banks and Customers

Digital onboarding in banking operates within a complex regulatory framework designed to prevent financial crimes while protecting consumer interests. Understanding these requirements is essential for successful implementation.

1. Know Your Customer (KYC) Regulations

KYC forms the foundation of customer due diligence in banking, ensuring identity verification, regulatory compliance, and mitigating fraud risk.

- Financial institutions must verify customer identities using reliable, independent sources

- Customer information must be regularly updated and monitored

- Risk-based approaches allow for proportionate verification based on customer profiles

- Non-compliance penalties have increased by 45% in recent years

Low-code advantage: Automated workflows and decision trees make it easy to trigger risk-based KYC flows, adjust verification steps, and log all actions for audit compliance.

2. Anti-Money Laundering (AML) Requirements

Digital onboarding must incorporate robust AML measures to detect suspicious activity, prevent financial crimes, and ensure regulatory compliance from the very first interaction.

- Screening against sanctions and watchlists

- Monitoring for suspicious transaction patterns

- Reporting suspicious activities to financial intelligence units

- Maintaining comprehensive audit trails for investigations

Low-code advantage: AML logic can be embedded directly into onboarding pipelines using configurable rules. Updates to blacklists or screening criteria are easy to roll out via visual admin panels, without hard-coding.

3. Regional Regulatory Frameworks

Digital customer onboarding in banking must adapt to various regulatory environments to ensure global compliance, reduce legal risks, and streamline cross-border customer acquisition.

Europe

- eIDAS Regulation provides a framework for electronic identification

- GDPR establishes strict data protection requirements

- 5AMLD and 6AMLD strengthen AML directives with specific provisions for digital verification

North America

- Bank Secrecy Act (BSA) and PATRIOT Act govern customer identification

- Federal Financial Institutions Examination Council provides digital banking guidance

- State-level regulations add complexity to uniform implementations

Asia-Pacific

- Countries like Singapore and India lead with progressive digital identity frameworks.

- China maintains stricter controls over digital financial services

- Australia's Anti-Money Laundering and Counter-Terrorism Financing Act includes digital verification provisions

Low-code advantage: Low-code platforms make it feasible to create region-specific onboarding workflows from reusable templates. This ensures banks can maintain compliance in multiple jurisdictions with minimal development overhead.

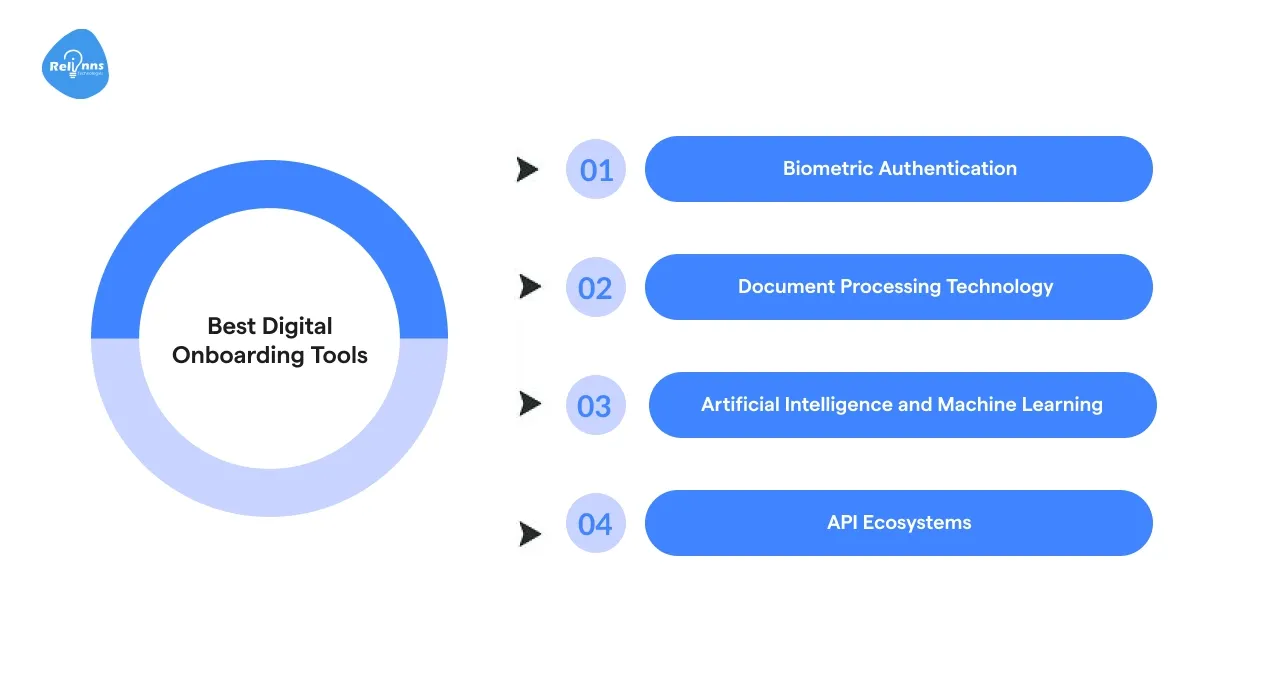

Best Digital Onboarding Tools and Low-Code Technologies for Banking Success

The effectiveness of digital onboarding in banking depends significantly on the technologies employed. Modern digital onboarding utilizes several advanced tools to create secure and efficient processes.

With visual builders, prebuilt integrations, and drag-and-drop workflows, low-code banking solutions empower teams to launch these tools faster, iterate without heavy coding, and ensure compliance across global markets.

1. Biometric Authentication

Biometric technologies have revolutionized identity verification in digital onboarding by providing secure, fast, and user-friendly methods, such as facial recognition and fingerprint scanning.

Low-code advantage: Platforms offer prebuilt connectors for leading biometric APIs (e.g., Face++, iProov), enabling integration within hours, without deep backend work.

- Facial recognition accuracy has improved by 20x since 2014 (Source: NIST)

- Fingerprint authentication is used by 64% of banks offering digital onboarding

- Voice recognition provides an additional security layer for phone banking

- Behavioral biometrics analyze typing patterns, device handling, and navigation habits

Financial institutions report an average 80% decrease in account takeover incidents after implementing behavioral biometrics, compared to traditional knowledge-based authentication methods. (Source: Nuance)

2. Document Processing Technology

Advanced document handling is central to digital customer onboarding banking, enabling seamless ID verification, data extraction, and compliance through OCR, AI, and secure upload workflows.

Low-code advantage: Tools like ABBYY or Google Cloud Vision integrate easily via REST APIs within low-code environments, drastically reducing setup and update time.

- Optical Character Recognition extracts data from ID documents with 98% accuracy

- Machine learning algorithms detect document tampering and forgeries

- Computer vision techniques verify security features in official documents

- Automated data matching cross-validates information across multiple sources

According to research in the International Journal of Management & Entrepreneurship Research, banks using AI-driven document automation processes can approve loans 70% faster, demonstrating a significant performance gain. (Source: ResearchGate)

3. Artificial Intelligence and Machine Learning

AI/ML technologies enhance various aspects of digital onboarding by automating identity checks, detecting fraud patterns, and personalizing user experiences in real time.

Low-code advantage: AI logic, like risk scoring and predictive analytics, can be embedded via reusable components, decision trees, or rule engines in platforms like Joget, OutSystems, or Mendix.

- Risk scoring models assess trust based on an individual's behavior and history.

- Anomaly detection flags irregular patterns that may indicate fraud.

- Predictive analytics suggest relevant services by anticipating needs.

- NLP enhances chatbot interactions for smoother onboarding experiences.

Financial institutions that utilize AI in onboarding experience a 25% improvement in risk assessment accuracy, thanks to enhanced predictive analytics and improved fraud detection. (Source: MarketWatch)

4. API Ecosystems

Modern digital onboarding in banking relies heavily on APIs to integrate identity verification, credit checks, and regulatory compliance seamlessly within existing banking systems.

Low-code advantage: Drag-and-drop API orchestration and prebuilt modules for services like Onfido, Trulioo, Experian, or DocuSign simplify integration timelines.

- Open banking enables secure user data sharing with consent.

- Third-party verification tools integrate easily for faster onboarding.

- Credit bureaus supply real-time credit and identity information.

- Digital signature providers ensure documents meet legal standards.

Approximately 75% of the top 100 global banks utilize public APIs, underscoring the importance of API integration in their digital strategies. (Source: Bai)

Best Practices for Successful Digital Onboarding in Banking using Low Code

Implementing effective digital onboarding in banking requires adhering to several best practices that strike a balance between security, compliance, and customer experience.

1. Design for Simplicity

User experience is paramount in digital customer onboarding banking, ensuring smooth navigation, fast processes, and minimal friction to boost conversions and customer satisfaction.

- Limit input fields to only essential details for a quick onboarding process.

- Break complex processes into smaller, logical, and manageable steps.

- Show users progress indicators to reduce confusion and abandonment.

- Utilize pre-fill options to expedite form completion and ensure accuracy.

- Implement innovative forms that adapt dynamically to user responses.

According to a HubSpot analysis of over 40,000 landing pages, forms with three fields averaged a conversion rate of ~25%. In contrast, those with seven fields dropped to around 21%, highlighting how the addition of extra fields significantly reduces conversions. (Source: Medium)

2. Prioritize Security Without Friction

Effective digital onboarding strikes a balance between robust security and usability, ensuring protection against fraud while delivering a smooth and intuitive customer experience across all touchpoints.

- Implement risk-based authentication that adjusts verification intensity

- Use invisible security measures that don't burden customers

- Provide clear security explanations to build trust

- Offer multiple authentication options for different customer preferences

- Test security measures with real users before deployment

83% of customers say they’re willing to share personal data for a more personalized experience if companies are transparent about how it’s used and keep it secure. (Source: Salesforce)

3. Continuous Optimization

Digital onboarding should evolve based on performance data, enabling continuous improvement through user feedback, analytics insights, and conversion rate optimization strategies.

- Track completion rates to identify where users abandon the onboarding journey.

- Analyze dropout points to identify and remove areas of user friction.

- A/B test verification steps to improve conversion and user experience.

- Gather customer feedback regularly and apply insights for refinement.

- Benchmark progress by comparing metrics against industry onboarding standards.

According to McKinsey, organizations implementing real-time analytics and continuous optimization experience 15–20% increases in conversion and completion rates compared to those using periodic analysis.

4. Omnichannel Consistency

Effective digital onboarding in banking provides consistent experiences across channels, ensuring seamless transitions between mobile, web, and in-branch interactions for greater user satisfaction and trust.

- Ensure seamless transitions between mobile and web onboarding interfaces.

- Allow customers to pause and resume onboarding across multiple devices.

- Maintain visual and functional consistency across all digital platforms.

- Provide consistent support options across every onboarding touchpoint.

- Synchronize customer data in real-time across channels and devices.

Sixty-four percent of customers expect companies to provide seamless experiences across channels, so they don't have to repeat themselves. (Source: Salesforce)

Examples of Banks Excelling at Digital Onboarding in 2025

Several financial institutions have established themselves as leaders in digital customer onboarding banking through innovative approaches and customer-centric design.

1. DBS Bank (Singapore)

DBS has revolutionized digital onboarding in banking through its mobile-first strategy, enabling instant account opening, e-KYC, and seamless customer experiences across Southeast Asia.

- Account opening was completed in under 5 minutes via the DBS digibank platform.

- Achieved 100% paperless onboarding with fully embedded eKYC process.

- Reached 90% straight-through processing rate for digital applications.

- Saw 40% increase in new accounts post-onboarding implementation.

DBS reports that customers acquired through digital channels have a 30% higher lifetime value than those acquired through traditional channels. (Source: DBS Annual Report)

2. Chime (United States)

This neobank has designed its entire business model around frictionless digital onboarding, focusing on speed, simplicity, and customer-centric experiences from the very first interaction.

- Two-minute account opening process with minimal user input required.

- No credit check requirements for faster and more inclusive onboarding.

- Early direct deposit access offered immediately after account setup.

- In-app ID verification enables real-time decisions and instant approvals.

According to Insider Intelligence, Chime was the most downloaded digital banking app in the U.S. in 2022, with over 10 million downloads, driven by its fast, easy mobile onboarding and no-fee model. (Source: Chime)

3. N26 (Europe)

N26 has set new standards for digital onboarding across European markets by offering fast, secure, and fully mobile account opening experiences backed by seamless eKYC and intuitive app design.

- Video identification option enables enhanced and secure user verification.

- Achieves eight-minute average onboarding time across supported regions.

- Multi-country compliance integrated into one seamless application workflow.

- Real-time translation of regulatory disclosures improves user clarity and compliance.

N26 reports that its fully digital model significantly reduces customer acquisition costs, citing lower marketing expenses and faster onboarding times compared to traditional banks. (Source: N26)

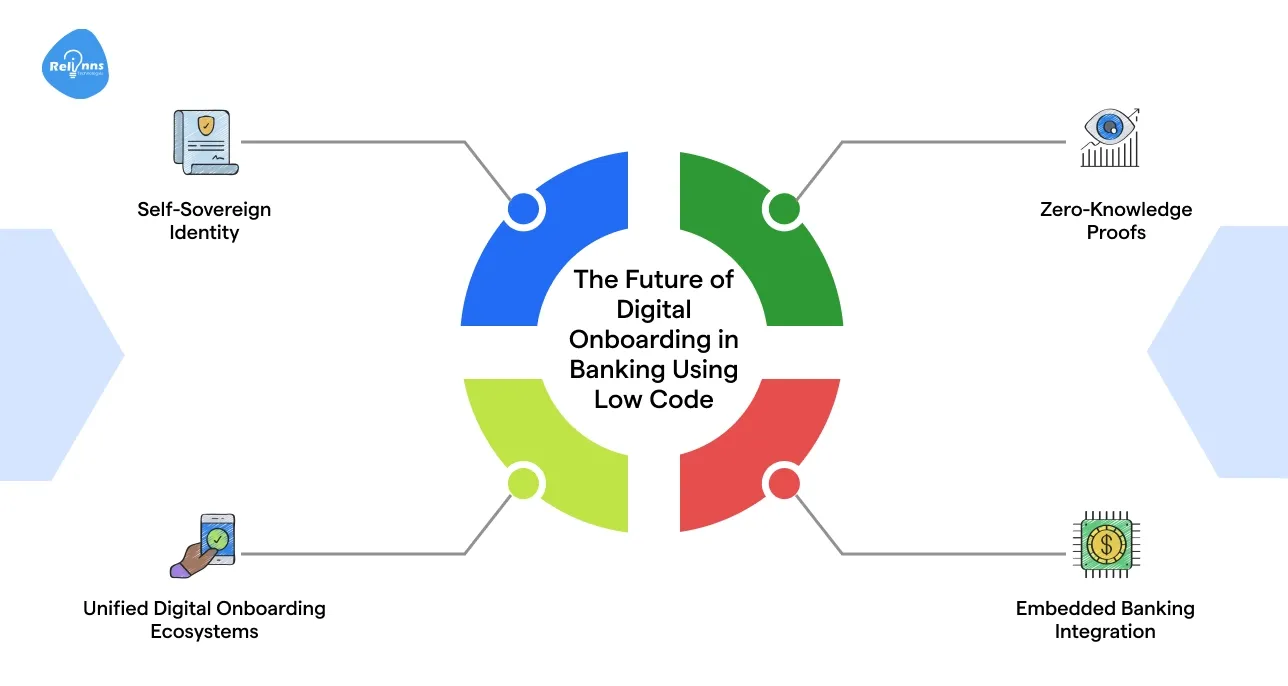

The Future of Digital Onboarding in Banking Using Low Code

Digital onboarding in banking is evolving rapidly, driven by rising customer expectations and technological advancements.

Emerging technologies will define the next phase, but low-code will be the foundation that makes them agile, scalable, and cost-effective.

1. Self-Sovereign Identity

The concept of customer-owned digital identity is gaining momentum, offering users greater control, privacy, and security in financial onboarding processes.

- Blockchain-based ID verification eliminates redundant, repeated KYC.

- Customers retain complete control over their identity credentials in a secure manner.

- Banks access only necessary data with explicit customer consent.

By 2026, 30% of global banking customers are expected to use some form of self-sovereign identity. (Source: Gartner Identity Management Forecast)

2. Zero-Knowledge Proofs

Advanced cryptography is enabling new verification approaches, such as zero-knowledge proofs, to enhance privacy, security, and trust in digital onboarding processes.

- Verification occurs without exposing any underlying sensitive user data.

- Proves identity attributes without revealing the actual attribute values.

- Enhances privacy while still maintaining full regulatory compliance standards.

Financial institutions implementing zero-knowledge approaches report 60% lower data breach risks. (Source: IBM Security Report)

3. Unified Digital Onboarding Ecosystems

The future holds interconnected verification networks that enable secure, cross-platform identity sharing, streamlining onboarding while reducing duplication, fraud risks, and compliance burdens across financial institutions worldwide.

- Shared KYC utilities enable seamless onboarding across financial institutions.

- Regulatory-approved digital IDs ensure secure and compliant customer verification.

- Standardized protocols reduce friction and support interoperable onboarding systems.

Industry consortia are already developing these solutions, with projected cost savings of $2-3 billion annually across the banking sector. (Source: McKinsey Financial Services Report)

4. Embedded Banking Integration

Digital onboarding is increasingly moving beyond traditional banking channels, extending into fintech apps, embedded finance platforms, and non-bank ecosystems to facilitate broader and more accessible customer acquisition.

- One-click account creation within apps enables instant access to financial services.

- Context-aware offers deliver personalized banking at the right moment.

- Background verification runs invisibly to streamline the user onboarding experience.

By 2025, 50% of banking relationships are expected to originate through embedded channels.

Real-World Success Stories On Digital Onbaording In Banking

Case: Bank Using Joget for Identity and Access Management

A leading Indonesian bank serving over 10,000 employees across 800+ branches aimed to streamline its identity and access management processes through digital transformation.

Challenges

- The manual, paper-based user ID request system caused delays and inefficiencies.

- Thousands of monthly access requests were hard to monitor, leading to SLA breaches.

- Lack of digital validation meant non-compliant forms couldn’t be auto-rejected.

- No centralized system to generate reports or track approvals.

- Manual handling by user administration team strained resources and increased fraud risk.

Solutions

- Implemented a digital Identity & Access Management Workflow using Joget.

- Integrated securely with core banking systems via middleware.

- Automated the request approval process for faster turnaround and compliance.

- Centralized all user ID requests and digitized submission and validation.

- Streamlined backend operations to reduce admin load and error rates.

Results

- Seamlessly handles over 1,000 access requests monthly with zero performance issues.

- Achieved 100% automation of key onboarding processes.

- Reduced manual workload and increased efficiency in backend operations.

- Enabled faster, error-free user ID provisioning with enhanced security.

- Boosted end-user satisfaction through a simplified, transparent experience.

What’s Next: Future of Digital Onboarding in Banking

As the digital landscape evolves, digital onboarding in banking is moving toward more autonomous, secure, and adaptable systems. Here’s a look at the four tech shifts shaping the future of digital customer onboarding banking.

Self-Sovereign Identity & Blockchain

Customer-owned digital IDs stored on blockchain will revolutionize onboarding by enabling instant KYC with full user control.

- Reduces redundant KYC across institutions

- Enhances privacy through decentralized data ownership

- Prevents data tampering with immutable blockchain records

Zero-Touch Onboarding

Customers will onboard without lifting a finger, AI and background verification will do the work.

- Passive identity verification with facial biometrics and device data

- Auto-form filling using stored credentials

- Invisible compliance checks in real-time

AI-Led Compliance

Machine learning will power proactive and dynamic compliance systems.

- Detects fraud through behavioral analytics

- Adjusts KYC intensity based on user risk level

- Reduces false positives through smarter screening

Rise of No-Code Builders

Banks will ditch heavy dev cycles in favor of visual tools for onboarding flow design.

- Rapid UI/UX adjustments without coding

- Rule changes deployable in hours

- Ideal for regional and regulatory adaptations

Conclusion: The Future of Digital Onboarding in Banking

Digital onboarding is no longer optional—it's the front door of modern banking. As AI, reusable IDs, and embedded finance evolve, low-code app development will be critical for building flexible, compliant, and fast-to-market onboarding systems.

Institutions that embrace low-code now will stay ahead in user experience, risk mitigation, and digital scale.

As AI, biometrics, and reusable digital identities reshape the finance industry, banks that prioritize both usability and security will thrive. Continuous optimization, performance analytics, and cross-platform consistency will separate market leaders from laggards.

The future belongs to institutions that make onboarding a frictionless, trusted gateway into long-term relationships.

Why Choose Relinns for Low-Code Banking Solutions?

- Save 70% costs with flexible developers at global outsourcing rates.

- Build fast using expert low-code/no-code development platforms.

- Launch MVPs quickly and validate ideas with real users.

- Agile development enables fast delivery and keeps budgets under control.

Frequently Asked Questions (FAQ's)

How can banks balance personalization with compliance in digital onboarding?

Banks can use AI-driven decision engines in low-code platforms to deliver tailored onboarding experiences while dynamically enforcing region-specific KYC and AML rules to ensure full regulatory compliance.

What role does chatbot automation play in digital banking onboarding?

AI-powered chatbots integrated into low-code workflows guide users through onboarding steps, resolve queries in real time, and personalize journeys without increasing support staff or compromising compliance.

How does low-code improve testing and rollout of new onboarding features?

Low-code platforms enable banks to run A/B tests, modify onboarding flows instantly, and roll out updates across channels—without writing new code or redeploying entire applications.

Can digital onboarding platforms support multilingual and regional compliance differences?

Yes. Low-code systems allow multilingual onboarding journeys and localization logic to adapt content, flows, and validation steps dynamically, ensuring compliance across multiple jurisdictions and customer bases.

How do digital onboarding tools integrate with credit decision engines?

Modern onboarding stacks connect to credit bureaus and scoring models via low-code APIs, enabling real-time eligibility decisions, product recommendations, and instant loan pre-approvals within onboarding.

What KPIs should banks track to measure onboarding success?

Banks should track completion rates, drop-off points, verification time, false positives, user satisfaction, and time-to-activate accounts. Low-code dashboards provide real-time visibility across these onboarding KPIs.